It is plausible that high-yield corporate bonds have return characteristics substantially different from those of other asset classes, and therefore represent a good diversification opprotunity. To check, we add iShares iBoxx $ High-Yield Corporate Bond (HYG) to the following mix of asset class proxies (the same used in “Simple Asset Class ETF Momentum Strategy”):

PowerShares DB Commodity Index Tracking (DBC)

iShares MSCI Emerging Markets Index (EEM)

iShares MSCI EAFE Index (EFA)

SPDR Gold Shares (GLD)

iShares Russell 1000 Index (IWB)

iShares Russell 2000 Index (IWM)

SPDR Dow Jones REIT (RWR)

iShares Barclays 20+ Year Treasury Bond (TLT)

3-month Treasury bills (Cash)

First, per the findings of “Asset Class Diversification Effectiveness Factors”, we measure the average monthly return for HYG and the average pairwise correlation of HYG monthly returns with the monthly returns of the above assets. Then, we compare cumulative returns and basic monthly return statistics for equally weighted (EW), monthly rebalanced portfolios with and without HYG. We ignore rebalancing frictions, which would be about the same for the alternative portfolios. Using adjusted monthly returns for HYG and the above nine asset class proxies from May 2007 (first return available for HYG) through April 2013 (72 monthly returns), we find that:

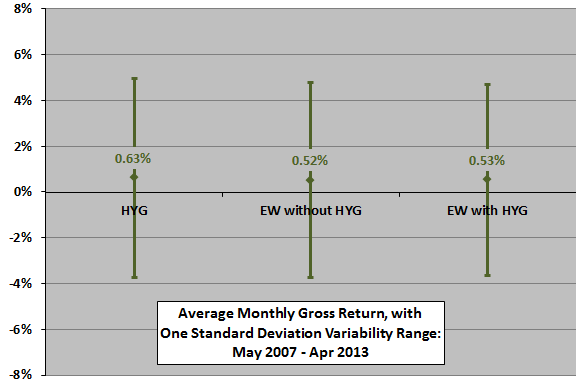

The following chart summarizes average monthly returns with variability ranges of one standard deviation for HYG and the EW portfolios without and with HYG over the available sample period. During this time, HYG generates an average return comparable to that of EW without HYG. Adding HYG to the diversified EW portfolio has little effect on return and volatility. The ratio of average return to standard deviation (return per unit of risk) is 0.12 (0.13) without (with) a HYG position.

The average pairwise correlation of HYG monthly returns with those of the other assets is a relatively high 0.45 over the available sample period, driven by strong positive pairwise correlations with equity assets.

Per “Asset Class Diversification Effectiveness Factors,” the above average return (high average pairwise correlation) of HYG indicates a reasonably good (poor) contribution with respect to portfolio diversification.

Sample size is small in terms of a variety of market conditions.

What is the net result of these effects?

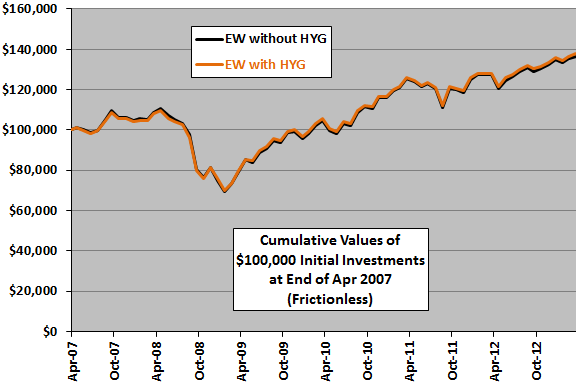

The next chart compares cumulative values of EW portfolios without and with HYG in the mix over the available sample period. Adding HYG appears to add a slight positive effect most of the time.

Again, sample size is small.

In summary, evidence from simple tests over a short available sample period does not support belief that adding a proxy for high-yield corporate bonds to a diversified portfolio has a material impact on overall performance.

It appears that HYG acts essentially as another equity position.

Cautions regarding findings include:

- As noted, the sample period is very short in terms of market conditions (one bear market and little variation in base interest rates).

- Including the trading frictions associated with monthly rebalancing would depress performance of both portfolios, depending mostly on portfolio size. When a portfolio of X assets performs just as well as one with X+1 assets on a gross basis, the former may be superior on a net basis.

See also “Testing Bond Allocation Strategies” and “Momentum Timing of Junk Bond Fund?”.