Trading Calendar – August

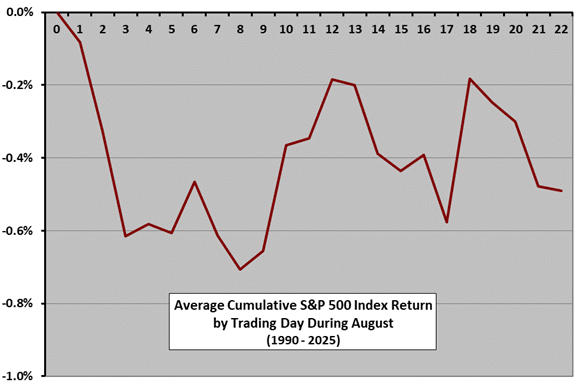

The following chart shows the average month-to-date percentage change in the S&P 500 index by trading day during August from 1990 through 2025. Day 0 represents the July close. It shows that the index during August tends to be a little weak, with a weak first half not recovered in the second half. We have not used data for trading day 23, because most Augusts do not have 23 trading days. Also, sample size is only 27-36 for specific trading days, so these results are only mildly suggestive rather than predictive. For 1990-2025, 21 Augusts have been winners and 15 losers.

Return to the Trading Calendar to find other monthly profiles.