Chapter 4: Accounting for Implementation Frictions

Investment frictions (costs) include such burdens as broker transaction fee, bid-ask spread, impact of trading (for large trades), borrowing cost for shorting, cost of leverage, costs of data, software and hardware for research, fund loads, cost of advisory services and cost of an investment manager.

These costs vary considerably by category of investor (retail or institutional), over time, across countries and across types of assets. For example:

Transaction fees vary by broker.

Transaction fees are generally higher percentage-wise for small trades than large trades, and therefore for investors with small accounts than those with large accounts. Sophisticated traders may be able to suppress frictions via broker arrangements and order placement algorithms.

Market liquidity tends to be lower in emerging markets than developed markets, generally indicating higher bid-ask spreads and impacts of trading in emerging markets.

Both transaction fees and bid-ask spreads were generally much higher in past decades than now due to regulatory changes (ending of fixed commissions and decimalization) and technological advances (lower cost of execution and lower barrier to entry for discount brokers). This variation is problematic for long backtests.

Frictions are generally higher percentage-wise for option trades than equity trades of similar sizes. Frictions for futures trades are comparatively low.

Frictions for aesthetic assets such as art and wine are very large compared to those for financial assets.

Cost of an investment manager subsumes the other costs (perhaps with economies of scale) but adds incremental fees for administration and management.

Realistic modeling of frictions is often very difficult, especially for samples spanning long time periods. Many researchers set a goal of analyzing gross risk premiums or anomalies and therefore ignore frictions in measuring returns and alphas (returns adjusted for widely accepted risk factors). However, research findings based on net results may differ substantially from those based on gross results, to the extent of rendering realistic implementations unprofitable. The following sections cover some considerations and approaches for modeling trading frictions.

4.1 Impact of Frictions

As discussed above, while investment frictions generally reduce returns, their impact is situational. For example, strategies that specify a large number of holdings to diversify against individual asset risks imply very small positions with high percentage-wise frictions for small investors (or, more realistically, force such investors to specialized funds with bigger scale but also material administration and management fees).

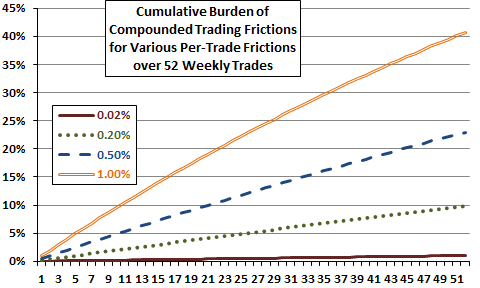

Strategies that generate high portfolio turnover due to frequent measurement of rapidly changing indicators generate rapidly compounding frictions that may substantially offset compounding gross returns. Figure 4-1 illustrates the cumulative burdens from compounding of several levels of frictions for weekly trading over one year. The annualized friction ranges from 1.0% for a per-trade friction of 0.02% to 40.7% for per-trade friction of 1.00%. When per-trade friction is not extremely low, comparing the performances of high-turnover (for example, price momentum) and low-turnover (for example, value) strategies based on gross returns can mis-rank strategies.

Figure 4-1: Compounding Effect for Weekly Trading Frictions

Strategies that preferentially select assets with exceptionally high frictions (such as small-capitalization stocks, low-volume assets or high-volatility assets) may perform well on a gross basis but not on a net basis. Such preferences may contribute to the size effect (small stocks tend to outperform large stocks), the value premium (stocks with high book-to-market ratios tend to outperform those with low ratios) and the momentum effect (stocks with high recent returns tend to outperform those with low recent returns), all generally estimated based on gross returns. Some studies avoid or mitigate this concern by excluding assets likely to have exceptionally high frictions from the universe considered.

Some studies identify high gross returns in old (pre-1990s) data and generate high “net” returns by applying current implementation frictions (low, such as the low-friction alternatives in Figure 4-1). If investors operating contemporaneously with the old data had access to low frictions, it is plausible that they would have exploited and suppressed or extinguished past asset mispricing. In other words, the level of investment frictions affects the speed of market adaptation and the magnitude of any residual mispricing.

Some studies ignore investment frictions by assuming exploitation of a mispricing discovered in past data via funds made available by a broker for “free” trading. Had such funds been available in the past, traders may have suppressed or extinguished the mispricing by using them. And, these funds may have some offsetting broker/fund manager fees reflected in fund returns. Investors trading these funds and therefore assuming zero frictions in backtests can mitigate the latter concern by using the returns of these funds since inception for strategy robustness tests.

4.2 Backtesting with Index Returns

Indexes do not account for frictions associated with changes in their component assets or periodic rebalancing (if not market capitalization-weighted), and therefore tend to overstate exploitable returns. Of particular concern are long samples, since tracking indexes may have been more costly decades ago. It is preferable to use assets (funds) to be traded rather than indexes themselves in backtesting strategies. However, index histories are generally longer than fund histories. One approach is to supplement backtests on indexes with shorter tests on tracking funds as a robustness check (applying appropriate frictions for any trading in and out of the indexes/funds). If the tracking funds are mutual funds, loads imposed would add to frictions and trading restrictions may conflict with strategy signal execution. Returns for funds applying loads and trading restrictions may not be achievable by unconstrained funds.

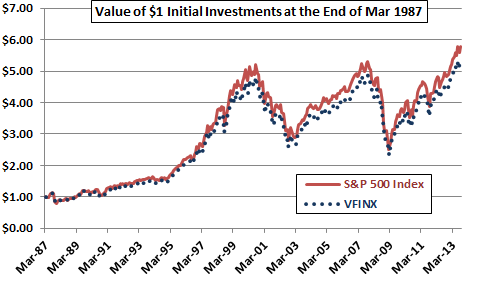

For example, Figure 4-2a compares the monthly closing cumulative values of $1 initial investments from the end of March 1987 through September 2013 in the S&P 500 Index and Vanguard 500 Index Fund Investor Shares (VFINX), which tracks the index (both excluding dividends). Data for both the S&P 500 Index and VFINX are monthly from Yahoo!Finance. The mutual fund generally lags the index, with the gap mostly growing over time. The terminal value of VFINX is about 8% lower than that for the index. The average monthly return for VFINX is 0.63% (compared to 0.65% for the index), with standard deviation of monthly returns 4.41% (compared to 4.42% for the index). The underlying assets in this case are liquid, and the effect of implementation frictions is therefore modest.

Figure 4-2a: S&P 500 Index vs. VFINX

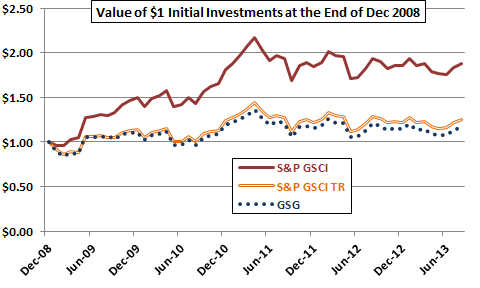

As a second example, Figure 4-2b compares the monthly closing cumulative values of $1 initial investments from the end of 2008 through September 2013 in each of:

- S&P GSCI, a production-weighted commodity index with value based on prices of the futures contracts included in the index.

- S&P GSCI Total Return (TR), which incorporates the returns of S&P GSCI, the return from “rolling” hypothetical positions in associated futures contracts forward as they approach delivery and interest earned from full collateralization of contract positions. The roll return (or roll yield) is often negative and reduces the index level.

- iShares S&P GSCI Commodity-Indexed Trust (GSG), an exchange-traded fund (ETF) designed to track the S&P GSCI Total Return Index before expenses.

Monthly levels of S&P GSCI and S&P GCSI TR are from S&P Dow Jones Indices LLC. Monthly prices for GSG are from Yahoo!Finance.

Average monthly returns for S&P GSCI, S&P GCSI TR and GSG are 0.36%, -0.41% and -0.50%, respectively, with associated standard deviations of monthly returns 7.49%, 7.16% and 7.28%. The terminal value for GSG is 38% lower than that for S&P GCSI and 7% lower than that for S&P GCSI TR. Using S&P GCSI to represent commodities in a strategy backtest would generate much more optimistic findings than using S&P GCSI TR, which in turn would generate a little more optimistic findings than using GSG.

Figure 4-2b: Commodity Index vs. Exchange-Traded Note

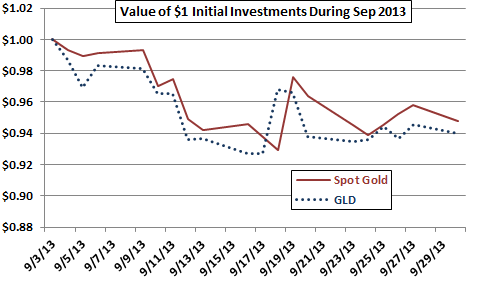

It can also be important to use tradable assets rather than indexes or spot prices in backtesting short-term signals. For example, Figure 4-2c compares the daily closing cumulative values of $1 initial investments in spot gold (London 3:00 p.m. Gold Fixing Price) and daily closes of SPDR Gold Shares (GLD) during September 2013. Data for spot gold prices are from FRED and for GLD are from Yahoo!Finance.

The average absolute difference in daily returns between spot gold and GLD is 1.3%, ranging as high as 4.1%. Mismatches in this case may derive from time of measurement, as well as implementation frictions. In any case, a trader backtesting a short-term trading strategy could be misled by using the spot price “index” rather than tradable asset returns.

Figure 4-2c: Daily Spot Gold vs. Daily GLD

4.3 Mitigating the Difficulty of Modeling Frictions

As noted above, investment frictions vary considerably by category of investor, over time, across countries and across types of assets, confounding their incorporation into strategy models. Two general approaches for mitigating this complexity are:

- For long-term backtests, break the sample into subperiods to compare gross strategy performance in high-friction and low-friction eras. If profitability is substantially lower during the low-friction era, then the assumption of zero frictions (not some exploitable edge) may be driving profitability during the high-friction era.

- Check the sensitivity of backtesting results for recent data to different assumed levels of friction to estimate the margin of safety with respect to aggregate implementation costs (which should consider any of the following that apply: broker transaction fee, bid-ask spread, impact of trading, borrowing costs for shorting, cost of leverage, costs of data, software and hardware, fund loads, cost of advisory services and cost of an investment manager).

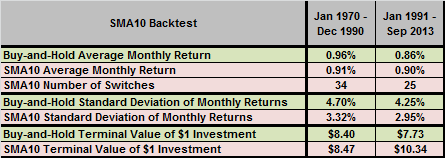

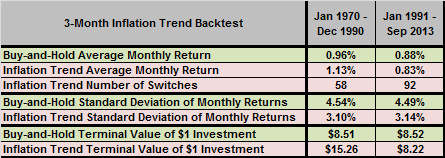

To illustrate the first approach, Tables 4-3a and 4-3b present results for backtests of two simple strategies applied to the S&P 500 Index during a high-friction era (January 1970 through December 1990) and a low-friction era (January 1991 through September 2013). Modeling inputs and assumptions are:

- S&P 500 Index levels are from Yahoo!Finance.

- Monthly dividend yields derive from Robert Shiller’s estimates (dividend divided by index level). Monthly reinvestment of dividends is frictionless.

- Return on cash while not in stocks is the three-month U.S. Treasury bill yield from Yahoo!Finance.

- Delay between signal and execution is zero (assuming slight anticipation of simple signals).

- Investment frictions and tax implications of trading are ignored.

If strategy performance is markedly stronger in the early subsample than the late subsample, then failure to account for frictions may explain the difference in performance (but other explanations are possible).

Under the hypothesis that the stock market is bullish (bearish) when a broad index is above (below) its 10-month simple moving average (SMA10), Table 4-3a presents summary statistics for a strategy that holds the total return S&P 500 Index (cash) when the index is above (below) its SMA10.

While not a particularly robust test (subsamples are not long in terms of number of independent 10-month measurement intervals), strong results in the late subsample indicate that signal effectiveness does not derive from ignoring trading frictions.

Table 4-3a: SMA10 Applied to the S&P 500 Index in High-friction and Low-friction Eras

Under the hypothesis that stocks react badly to a rising inflation rate, Table 4-3b presents summary statistics for a simple strategy that holds the total return S&P 500 Index (cash) when the three-month trend in the U.S. inflation rate is zero or negative (positive). The three-month trend in inflation is the slope of inflation rate versus time over the past three months. Since the Bureau of Labor Statistics generally releases new inflation data at mid-month, return measurements are from the 11th trading day of one month to the 11th trading day of the next month. This approach complicates calculation of returns but avoids looking ahead by a half month or waiting a half month to implement new information.

For this strategy, the relatively weak performance in the late subsample raises a concern that ignoring trading frictions is crucial to signal effectiveness. In fact, imposing a one-way switching friction of 1% eliminates signal effectiveness in the early subperiod based on average monthly return and terminal value.

Table 4-3b: Three-month Inflation Trend Strategy Applied to the S&P 500 Index

in High-friction and Low-friction Eras

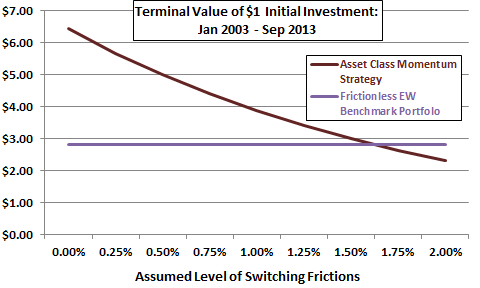

To illustrate the second approach, Figure 4-3 summarizes the effect of varying the assumed level of switching frictions (essentially transaction fee plus bid-ask spread in this case) on the terminal value of the simple asset class momentum strategy used in Figures 1-1, 3-0, 3-3b, 3-3c and 3-3d. This strategy switches each month to the one of nine asset class proxies with the highest total return over the past five months. The figure also shows the terminal value of an equally weighted and monthly rebalanced portfolio of the nine asset class proxies as a benchmark (calculated with no rebalancing frictions, so it conservatively includes a margin of safety in benchmark performance).

Results indicate that the active momentum strategy beats the passively rebalanced benchmark as long as switching friction is below about 1.5% of the portfolio balance. Actual switching frictions over the sample period are typically much lower than 1.5%, supporting belief in strategy usefulness.

Figure 4-3: Asset Class Momentum Strategy Friction Sensitivity Analysis

4.4 Summary

Key messages from this chapter are:

- The interplay of investment frictions with gross strategy returns is complex, with much research simply ignoring the frictions in calculations. Unless clearly specified otherwise, investors should assume that what they see is what they get before they pay the market for its services.

- Investors should look for strategies that provide a large margin for error in estimating the impact of investment frictions on profitability.

- Charlatans who want to sell amazing trading strategies should snoop for short-term signals that generate good gross return statistics (try assets with volatile returns), ignore the rapidly compounding drag of frictions on these returns, and then market to investors who did not read this chapter and the preceding one.

Next, Chapter 5 addresses the risk of market adaptation, whereby competitive pressures tend to suppress or extinguish exploitable return anomalies.