Chapter 5: Checking for Market Adaptation

The market is a complex system with many interacting parts, and external influences. As in other social settings, there are two aspects to market evolution: (1) adaptation to changes in external influences; and, (2) adaptation to adjust internal imbalances.

External influences include economic forces, political shifts, monetary policies, regulatory initiatives and information technology enhancements. For example:

- Economic globalization broadens the universe of assets available in the market, but tends to increase co-movement of assets.

- Political shifts may favor one industry over another or affect portfolio-level after-tax profitability of investing.

- Loose monetary policy may favor the financial industry.

- Regulatory actions on broker fees, quote granularity, short selling and margin levels impact investment frictions (profitability of trading) and cash requirements (portfolio-level returns).

- Mass availability of historical data and investing knowledge, computing power, analysis software and real-time trading accelerate market identification of and response to all market opportunities.

Investor adaptation to such influences is generally strategic.

Some investors continuously strive to identify and exploit internal market imbalances (pricing anomalies) through fundamental and technical analysis, both asset-specific and marketwide. They express perceived imbalances in different ways, such as:

- Undervalued versus overvalued

- Overbought versus oversold

- Too fearful versus too complacent

- Risk-on versus risk-off

- Informed versus noise

When many investors compete in exploiting an imbalance, they supply negative feedback that suppresses it. When more investors compete, suppression is faster. More generally and abstractly, acts of exploiting characteristics of an inferred distribution of investing returns change the distribution. (There is an extensive body of countering research that attributes perceived internal market “imbalances” to rational equilibriums based on actual, but sometimes subtle, risks. The counter-counter is a proposition that people are not even grossly rational, let alone subtly rational.)

The following sections discuss ways to detect and deal with market adaptation.

5.1 Detecting Market Adaptation

A simple test for market adaptation is assessment of strategy profitability across multiple subperiods to detect a trend. Four potential test outcome scenarios are:

- Persistence (or improvement) in gross or net profitability suggests that others have not yet discovered the strategy or that the underlying anomaly somehow resists market adaptation (perhaps due to some strong behavioral bias).

- A sharp decline in gross or net profitability suggests the appending of live data to a backtest that involved considerable snooping and therefore upwardly biased returns.

- A steady decline in gross or net profitability could mean that the market is adapting, with an increasing number of investors discovering and chipping away at the targeted alpha.

- Depending on the sample period, a steady decline in gross profitability could derive from falling investment frictions, with an anomaly that was not practically exploitable in old data becoming increasingly exploitable. As discussed in Chapter 4, ruling this scenario in or out by estimating net profitability of a strategy over long sample periods is problematic, because modeling investment frictions over time is extremely difficult. For short sample periods, this scenario may not apply.

Some studies test for market adaptation to asset pricing anomalies by comparing the gross profitability of strategies that exploit them before and after publication. These studies find that most anomalies weaken after publication, likely due to some combination of the second, third and fourth scenarios.

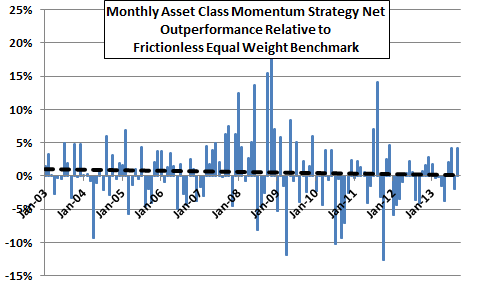

As an example, Figure 5-1a tracks the monthly net outperformance of the simple asset class momentum strategy used in Figures 1-1, 3-0, 3-3b, 3-3c, 3-3d and 4-3 during January 2003 through September 2013 (129 months). This strategy shifts each month to the one of nine asset class proxies with the highest total return over the past five months. Net performance assumes a switching friction of 0.25% whenever the strategy switches assets. Outperformance is relative to a benchmark consisting of an equally weighted portfolio of the nine asset class proxies considered in the strategy, frictionlessly rebalanced each month. The figure also shows a best-fit line indicating the trend in outperformance (dark dashed line). This line slopes downward from left to right. The downward slope suggests that the pool of alpha the strategy is designed to exploit is less and less available over time.

However, the downward slope could also be due to appending of live data to a snooped backtest with upwardly biased performance. Moreover, based on sample size in relation to the momentum ranking interval and variability in monthly outperformance, the trend is suggestive rather than compelling.

Figure 5-1a: Trend in Simple Asset Class Momentum Strategy Outperformance

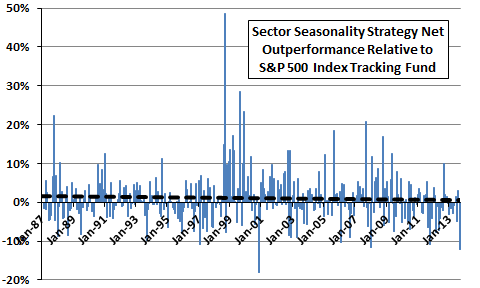

As a second example, Figure 5-1b tracks the monthly net outperformance of a sector seasonality strategy summarized on CXOadvisory.com that shifts among three U.S. equity sector mutual funds (technology, energy and gold mining) and cash according to the month of the year during February 1987 through September 2013 (320 months). There are no switching costs for these mutual funds. Outperformance is relative to a fund that tracks the S&P 500 Index. The best-fit trend line (dark dashed line) again slopes downward from left to right, though not as steeply as in Figure 5-1a. This seasonal strategy appears to more persistently effective than the simple asset class momentum strategy.

Again, the reason for the downward slope could be the appending of live data to a snooped backtest with upwardly biased performance, rather than market adaptation. Given the annual cycle underlying the strategy and the variability in monthly outperformance, this result also is suggestive rather than compelling.

Figure 5-1b: Trend in Sector Seasonality Strategy Outperformance

Just dividing a sample into halves or thirds might be revealing. Table 4-3a indicates that a simple strategy that holds the S&P 500 Index (cash) when the index is above (below) its 10-month simple moving average works at least as well on a gross basis during a recent low-friction era (January 1991 through September 2013) as during the preceding high-friction era (January 1970 through December 1990). While not a particularly robust test (subsamples are short relative to the 10-month signal measurement interval), strong gross results in the late subsample despite lower trading frictions suggest no market adaptation.

5.2 Resisting Revisionism

A more subtle aspect of market adaptation is the plausible argument that significant anomalies are much easily found in old data than new data with modern research tools and databases. And, in fact, the anomalies were practically undiscoverable by contemporaneous investors, who did not have the information technology to collect and process the requisite data. If contemporaneous investors could not discover an anomaly, was it an anomaly?

In other words, investors today are analytically more powerful than past investors and can discover and exploit anomalies their predecessors could not. Investors today are not analytically more powerful than current peers, who are competing to discover and exploit new anomalies. Investors today are less analytically powerful than their future competitors, who would easily consume today’s anomalies.

This thought progression suggests that current alpha is more elusive than indicated in historical data and will continuously evolve toward greater elusiveness as investors grow analytically more powerful and numerous. Potential mitigations are:

- Require an extra margin of strategy outperformance to account for (possibly accelerating) market adaptation.

- Periodically retest all strategies in use to detect market adaptation. A prudent working assumption is that any publicly known strategy has a useful life of no more than a few years.

5.3 Anti-Adaptation, the Persistence of Diversity

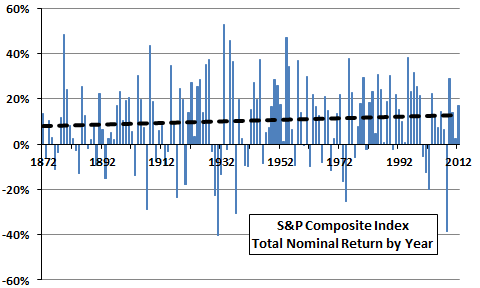

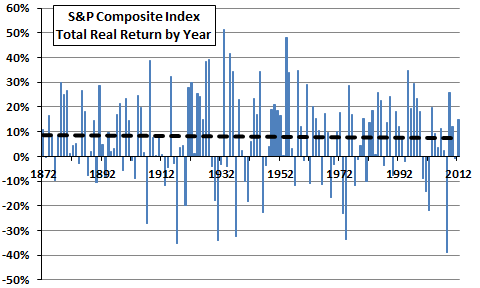

Figures 5-3a and 5-3b show the annual total nominal and real returns, respectively, for Robert Shiller’s S&P Composite Index during 1872 through 2012, along with best-fit linear trend lines (dark dashed lines). Data are from Robert Shiller’s Online Data. The nominal return trend line is upward-sloping, indicating that the nominal annual return on the U.S. stock market increases from 7.8% to 12.8% over the sample period. The real return trend line slopes slightly downward, indicating that the real annual return on the U.S. stock market slips from 8.7% to 7.5% over the sample period. Why do the specific market adaptations that substantially erode individual anomalies not translate into substantial erosion of overall market returns?

Results suggest that the aggregate market evolves from old to new sources of return on approximately replacement levels, regardless of internal anomalies. Those who buy and hold a broad market index therefore earn the average market return over long horizons. Those who continually shift focus from anomaly to anomaly have a firm benchmark.

Figure 5-3a: Trend in S&P Composite Index Annual Total Nominal Returns

Figure 5-3b: Trend in S&P Composite Index Annual Total Real Returns

Also, somewhat in opposition to market adaptation, markets seem to be very forgiving of “errors” and “irrelevancies” and “irrationalities.” For example:

- There is a persistent supply of new (uninformed) investors, and some investors persist in inferentially “incorrect” beliefs.

- Poorly performing funds can remain in business for years.

- Unreliable market forecasters and market indicators can attract attention for years.

The resistance to adaptation indicated by the second and third points relates to the difficulty of distinguishing skill from luck in investing. Learning in a noisy environment incorporates randomness. In such a situation, it is plausible that beliefs tend to be widely dispersed and resistant to correction.

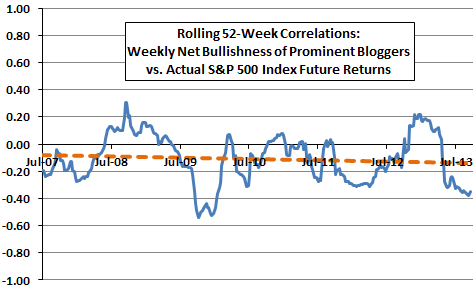

For example, Figure 5-3c from an analysis on CXOadvisory.com shows the 52-week rolling Pearson correlation during July 2007 through September 2013 between:

- The weekly net bullishness of a group of financial bloggers (percent bullish minus percent bearish) regarding the U.S. stock market over the next month; and,

- Actual return of the S&P 500 Index over the next four weeks.

A strong positive (negative) correlation indicates that the investors are net bullish or net bearish at the right (wrong) time. The figure also shows the best-fit trend line for the correlation (dashed line). Results indicate that the group is a little more wrong than right (average correlation is -0.11) and that group forecasting performance does not improve over time (the trend line tilts slightly downward). Though not accurate and not learning in aggregate, forecasting persists (more than six years, and counting).

Figure 5-3c: U.S. Stock Market Forecasting Acumen of a Group of Financial Bloggers

In fact, diversity of beliefs seems essential to market operations. There may be an analogy to biological evolution. The system characteristics that support/encourage diversity (random drift) are strong enough to balance system tendencies to optimize (convergence via natural selection), thereby strongly resisting non-adaptive stasis. In other words, the adaptive process in financial markets appears to be very messy, reliably preserving a wide diversity of investor beliefs. This diversity supports emergence of some anomalies, but not necessarily the same ones at all times.

An alternative interpretation is that the “errors” and “irrelevancies” and “irrationalities” are hypotheses awaiting evidence from wild distributions. They appear erroneous or irrelevant or irrational in the context of an incorrectly assumed tame (normal-like) distribution. In other words, expected return distributions are wilder than those posited in “traditional” finance models and assumed in identifying and exploiting anomalies. The models of behavioral finance, delineating rational and irrational behaviors, address this underestimation of wildness with inelegant patches.

5.4 Summary

Key messages from this chapter are:

- Investors should assume that financial markets pervasively adapt to suppress pricing anomalies and therefore: (1) favor only strategies with an outperformance margin; and, (2) periodically retest favored strategies.

- Investors should not despair that market adaptation will suppress overall opportunity.

- Charlatans selling trading strategies should blame market adaptation (rather than snooping and neglect of investment frictions) when a strategy does not work. Then sell the next strategy.

There are important differences between a strategy that exploits an anomaly and a portfolio. Success with the former does not guarantee success with the latter. Chapter 6 addresses this issue.