Chapter 6: Modeling at the Portfolio Level

Evaluating strategies based only on trade-level performance, as often presented by trading advisory (“education”) services, may mislead. Some strategies concentrate opportunities, at times identifying more trades than can reasonably be addressed with a limited amount of capital and at other times identifying no trades.

Moreover, evaluating strategies based only on a list of closed trades, with the performance of contemporaneous open trades unknown, may mislead because open trades may be losers that at times absorb all the capital and preclude further trading.

Modeling profitability at the portfolio level in such cases may be complicated and tedious, but is essential for understanding effects of a trading strategy on wealth. Portfolio-level modeling means carefully accounting for the allocations of all capital in a portfolio at all decision points in time series.

6.1 Feast or Famine Portfolios

For example, suppose an investor decides that portfolio capital reasonably accommodates no more than 10 positions (a trade-off between diversification and frictions). In a backtest, a trend-based signal that produces attractive trade-level performance generates an average of 20 open opportunities, varying from zero (very bad market state) to 30 (very good market state). When the number of opportunities is less than 10, the investor’s portfolio is partly or wholly in cash awaiting new opportunities. When the number of opportunities is greater than 10, the investor is fully invested in the first ten available. In calculating portfolio-level returns, the investor must take into account the returns on both active positions and residual cash.

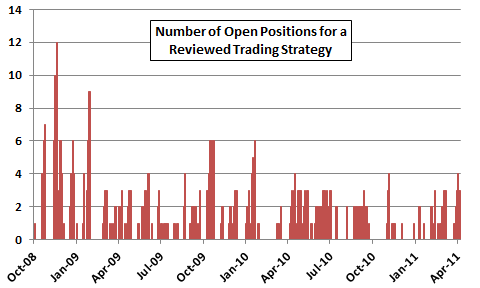

Figure 6-1 depicts the variation in short-term trading opportunities from mid-October 2008 through late April 2011 presented by an actual trading advisory service reviewed on CXOadvisory.com. Trading opportunities do cluster. Suppose an investor subscribes to the service with a plan of allocating about one quarter of capital to each position. With this constraint of no more than four open positions, the average number of active positions over time is 1.0 per day. The portfolio is therefore on average in active positions 25% of the time and in cash (awaiting new active opportunities) 75% of the time. The portfolio is completely in cash 55% of the time. The portfolio misses about a tenth of all trades because no more capital is available. Since return on cash is near zero during the sample period, the performance of the active trades must be extremely good to support a good portfolio-level return. Without the context of a portfolio-level implementation, the per-trade performance statistics are not very meaningful.

In fact, this discussion simplifies analysis, because some positions are short, and capital requirements for short positions may differ from those for long positions.

More specifically, assessing the strategy requires stepping through the time series of trades by:

- Setting an initial portfolio capital level

- Creating rules for incremental allocation of capital to trading opportunities

- Skipping any opportunities presented when fully invested

- Estimating and debiting per-trade frictions

- Amortizing the advisory fee over executed trades

- Estimating return on cash

For the actual review associated with Figure 6-1, this process generated a loss over the sample period, even though some per-trade gross return statistics seem good (see Section 8-2).

Figure 6-1: Number of Open Positions for a Short-term Trading Strategy

An ironic aspect of such trading strategies is that the best signals (those with the highest returns) may tend to come late within clusters (near market turning points). In other words, the very best trades are the least accessible to real, capital-constrained exploitation. In such situations, trades missed due to capital constraints make average performance of executed trades worse than the average performance of all trades signaled.

Further, if the portfolio employs leverage, there is a potential for margin calls and a requirement for a “shadow cash reserve” that the investor should include in modeling portfolio-level performance.

For the short-term trading strategy depicted in Figure 6-1, the advisor reports all trades. Assessing strategies for which the advisor reports only closed trades, while withholding information on open trades, is especially problematic.

6.2 Bow Wave Portfolios

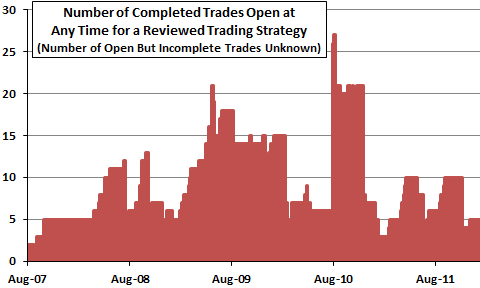

Trading advisory services that offer the performance of closed trades as proof of strategy effectiveness, while not disclosing the status of contemporaneous open trades, may mislead in two ways. First, it may not have been possible, as in Figure 6-1 above, to exploit all the closed trades based on realistic rules for allocating portfolio capital. Second, a “bow wave” of open trades (pending some signal or expiration date) may depress real-time portfolio-level returns and tie up capital in poor trades.

Figure 6-2 depicts the variation in intermediate-term trading opportunities based on closed trades only from mid-August 2007 through late April 2011 presented via an actual trading advisory service reviewed on CXOadvisory.com. The average holding period for these opportunities is 57 calendar days. Suppose an investor subscribes to the service with a plan of allocating about one tenth of capital to each position. With this constraint of no more than 10 open positions, the average number of active positions over time from among these closed trades is 7.4 per day. Based on closed trade information only, the portfolio would be on average in active positions 74% of the time and in cash (awaiting new active opportunities) 26% of the time.

However, this strategy has unspecified positions that open but never close during the sample period, presumably because they have not met some profitability target or reached some other expiration condition. A time series portfolio-level analysis would include these open positions (marked to market) in calculating monthly, quarterly or annual portfolio returns.

The bow wave of open positions may absorb all portfolio capital for a substantial part of the sample period and preclude further trading. In other words, capital may often be “locked up” in the poorest trades.

Figure 6-2: Number of Open Positions for an Intermediate-term Trading Strategy

In general, evaluation of strategies that generate clustered trading signals for many assets requires time series analysis at the portfolio level as described in Section 6.1. It is not possible to evaluate with confidence a strategy with overlapping trades, some closed and some open, without information on the open trades.

6.3 Summary

Key messages from this chapter are:

- Investors focused on building wealth (rather than the thrill and agony of trading) should model strategy performance at the portfolio level.

- Portfolio-level modeling is essentially a time series accounting of all capital in the portfolio.

- Charlatans selling trading strategies should focus on gross performance statistics of closed trades for heavily snooped trading rules, obscuring the obstacles to building wealth at the portfolio level.

A drag on portfolio outcome not covered in Chapters 3 through 6 is taxes, perhaps the most difficult to assess. Chapter 7 addresses some relevant points on taxes.