Chapter 7: Thinking about Taxes

To the extent that governments tax different kinds of income/investment returns (interest, dividends, long-term capital gains and short-term capital gains) differently, taxes may be decisive for some individuals in designing a strategy or selecting one strategy over another.

Taxes are more personal than other investment frictions. Relevant questions include:

- What is the investor’s expected marginal tax rate?

- Does the investor have any capital losses carried forward from prior years that may offset future gains?

- Are the funds in a tax-advantaged account, such as (in the U.S.): a conventional Individual Retirement Account (IRA), subject to tax rates at the time of withdrawal (whatever they may be); or, a Roth IRA, subject to no taxes at withdrawal (as the rules stand now)?

An obvious risk to long-term strategies including assumptions about taxes is that governments may change the rules at any time.

The next two sections explore how incorporating tax avoidance into an investment strategy might impact returns.

7.1 Constraining an Intermediate-speed Strategy

Suppose a U.S. investor wants to “slow down” the signals for the simple asset class momentum strategy used in Figures 1-1, 3-0, 3-3b, 3-3c, 3-3d, 4-3 and 5-1a to replace short-term capital gains with long-term gains. Instead of shifting each month during January 2003 through September 2013 (129 months), this slow strategy shifts only each year to the one of nine asset class proxies with the highest total return over the past five months. Slowing the strategy down in this way both suppresses switching frictions (0.25% whenever the strategy switches assets) and eliminates short-term capital gains. However, because positions are in place for 12 months, the slow strategy may be very sensitive to month of initiation.

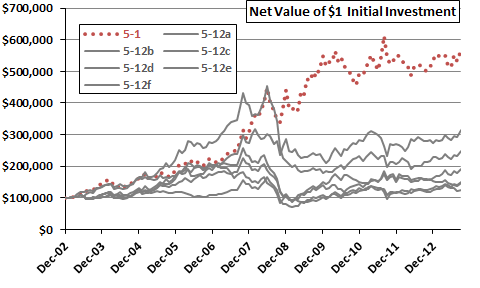

Figure 7-1 shows the net cumulative performances of six variations of the slow asset class momentum strategy (5-12a through 5-12f), all commencing in January 2003 but initiating 12-month holding cycles in six different months. The figure also shows net cumulative performance of the basic strategy that re-evaluates the top holding monthly (5-1). Net means accounting for switching frictions, but not taxes. The slow strategy, by design, trades infrequently (12 or fewer switches, compared to 51 for monthly re-evaluation). Over the entire sample period, all of 5-12a through 5-12f substantially underperform 5-1, essentially because they provide little or no crash protection in 2008. In this case, altering the basic strategy for tax advantage conflicts with the way the strategy works and is very counterproductive.

Figure 7-1: Slow Asset Class ETF Momentum Strategy

The results in Figure 7-1 suggest that, if the capital gains tax rules are very important to an investor, the investor should perhaps focus on slow-moving strategies, such as those based on long-term simple moving averages or fundamental valuation.

7.2 Constraining a Slow-speed Strategy

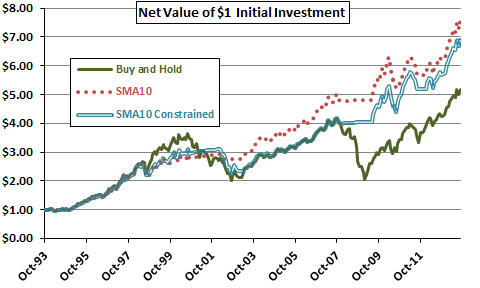

Suppose a U.S. investor uses the 10-month simple moving average (SMA10) to time the U.S. stock market, proxied by SPDR S&P 500 (SPY). Whenever dividend-adjusted SPY is above (below) its SMA10 at the end of the prior month, the strategy holds SPY (cash). However, to minimize tax impacts, the investor rejects any sell signal that falls within one year of the last purchase. The return on cash is the yield on 13-week U.S. Treasury bills (T-bills) and the friction for switching between SPY and cash is 0.125%. Data for SPY and the T-bill yield are from Yahoo!Finance.

Figure 7-2 shows the net cumulative values of $1.00 initial investments for buying and holding SPY, timing SPY with SMA10 (SMA10) and timing SPY with SMA10 constrained for tax purposes (SMA10 Constrained) since inception of SPY. Terminal values are $5.16, $7.52 and $6.88, respectively. Average monthly net returns are 0.79%, 0.89% and 0.87%, respectively, with standard deviations of monthly returns 4.37%, 3.02% and 3.36%. While SMA10 Constrained lags behind SMA10 for much of the sample period, it mostly beats buying and holding SPY. The tax advantages of SMA10 Constrained may offset underperformance relative to SMA10.

Figure 7-2: Constrained SMA10 Timing of SPY

7.3 Summary

Key messages from this chapter are:

- There are many complexities and uncertainties regarding interplay of investment returns and tax obligations, such that investors should probably focus more on returns than taxes.

- Investors who are tax-sensitive but interested in active strategies may want to focus on slow-moving ones.

- Charlatans selling trading strategies should focus on fast-moving, heavily snooped rules and ignore tax implications of trading.

Chapters 1 through 7 address a range of issues in investment strategy modeling. Chapter 8 illustrates some practical approaches to avoiding or mitigating them.