Chapter 9: Getting Expert Advice (Delegating Strategy Development)

Section 8-2 examines in detail the attractiveness of a short-term trading strategy offered in the quasi-advisory (“educational”) marketplace. Assessing this strategy entails considerable work, only to find that it is not attractive. This chapter covers more broadly the delegation of investment strategy development, ranging from following an expert’s public advice on market timing to deposit of funds for professional management. Such practices relieve investors (at a cost) of some or all of the burdens of learning, data collection/analysis, strategy design and disciplined implementation.

However, such delegation entails agency issues (conflicts of interest). Potentially more than they want to help their readers/subscribers/clients earn exceptional investment returns:

- Media that present investing advice want subscription fees or attention to advertisements. Media company interest in the usefulness of what they present is arguably secondary to attracting attention. In general, contributors to free media also have motives that bias what they present (attracting their own subscribers or clients).

- Academics studying financial markets want employment (and tenure) and funding of future research. They therefore must attract the attention of peers and publishers. They often have no stake in whether their research findings are useful to investors. They do have an incentive to attract the attention of investors when making a transition to investment management.

- Expert equity analysts want employment by brokers and asset managers, and access to industry sources. The interests of their bosses may not always coincide with the interests of the clients of their bosses or other investors.

- Newsletter sellers want subscription fees. Getting the attention of potential subscribers is essential to their business model. They sometimes seek attention by uncritically presenting snooped, gross trading system results as an “educational” service.

- Financial advisors want advisory fees. They must attract the attention of potential clients. As with newsletter sellers, the font used for marketing copy is much larger than that used for the legal disclaimer.

- Investment managers, mutual fund managers and hedge fund managers want management fees, normally as a percentage of account balance. They have to get the account before they can debit the balance. They have to get the attention of a potential clients before they get the account.

A common motive across the range of investment service providers is attention-seeking, which tends to drive offerors toward extreme representations (possible but low-probability scenarios, the tails of the distribution of potential outcomes). The most extreme representations offer the “holy grail” of amazingly large and reliable returns (appealing to investor greed) or the “safety of Noah’s ark” from impending doom (appealing to investor fear).

Conflict-of-interest materiality persists because investors have great difficulty distinguishing luck from skill when outcomes involve a high degree of randomness.

9.1 Investing Expertise?

There is a broad and deep stream of research on aggregate and individual investing expertise. Much of the analysis focuses on disentangling luck and skill. There are parallel research streams on the forecasting abilities of economic, financial and political experts. A reasonable interpretation of these streams is that experts in aggregate do not outperform reasonable benchmarks. An investor delegating investment strategy to the average expert therefore will likely not beat and (because of the expert’s fee) may well underperform a benchmark that is fairly easy to mimic.

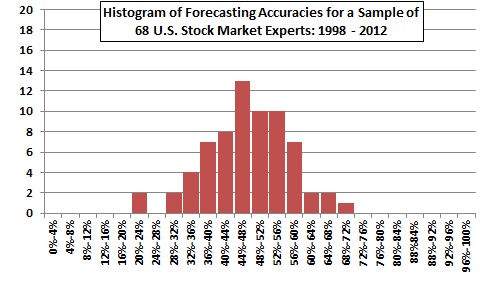

In a modest contribution to research on investing expertise, CXO Advisory Group LLC collected during 2005 through 2012 about 6,500 forecasts for the U.S. stock market made publicly by 68 experts (self-proclaimed or endorsed by publications). The assessment methodology includes normalization to an expected 50% accuracy in the absence of forecasting ability. The aggregate accuracy across all experts over the entire sample period is about 47%, a level very stable over most of the study’s duration. Figure 9-1 shows the distribution of accuracy rates across individual experts, ranging from about 30% to about 70% (some individual samples are small).

Figure 9-1: Histogram of U.S. Stock Market Expert Forecasting Accuracies

Why is aggregate forecasting accuracy so poor? Letting some of the experts speak for themselves (to the forecast grader):

- You took my statement out of context, leaving out forecast conditions and qualifications. Your judgment is unfair.

- I was close enough. You should give me credit.

- I will be right eventually; I just don’t know when. (Or: I was right, but my timing was off.)

- I may be wrong on some little things, but I’m right on all the big ones. The big ones far outweigh the little ones.

- I provide risk assessments based on historical tendencies, not forecasts. You should not call it wrong. The low probability scenario happened; it was just bad luck.

- My public statements may be sometimes wrong, but I am much more accurate in my private newsletter. You have to pay for truly valuable advice.

- Since I am rich and famous, I must be smart. Since I am smart, I must be right. No need to check up on me.

- If brokers weren’t so manipulative and investors so gullible, what I said would happen would have happened.

- The Plunge Protection Team (or the President, or the Vice President and his cabal, or the Treasury Secretary, or the Federal Reserve, or the prime brokers, or the Japanese, or the Chinese, or the EU) intervened to prop up the market.

- I was not wrong. You are an ass.

- You are just trying to make everyone else look bad so people will subscribe to your service.

The motive of forecasters to attract attention and therefore make extreme forecasts may work against forecasting accuracy.

Is it inevitable that the entanglement of skill and luck, in combination with attention-seeking behavior, will perpetually confound investors seeking expert help?

9.2 Due Diligence in Screening Experts

Screening the universe of investment “educators,” advisors and managers is somewhat like screening stocks. There are fundamental indicators (logic and plausibility of methods) and technical indicators (performance history). However, the former indicators are often vague and the latter generally unaudited (and sometimes hypothetical and gross of investment frictions).

Many experts offer testimonials as proof of value. However, testimonials are not a fair sample. They likely are unrepresentative, reporting only the most satisfied tail of the distribution of client experiences. Moreover, testimonials may be vague, and they may not come from particularly informed investors.

One step investors can take to screen investment experts is to find and read any legal disclaimers of the experts, which typically contain cautions such as:

“Past performance is no guarantee of future results.” [Investors might reasonably interpret the stream of research on performance persistence, such as for mutual funds and hedge funds, to indicate that persistence of outperformance is rare and persistence of underperformance is less rare.]

“It should not be assumed that the methods, techniques, or indicators presented in these products will be profitable.” [Such a statement is a stronger disclaimer than “no guarantee.” It is reasonable to infer than any investor buying the products does not believe this disclaimer.]

“Hypothetical or simulated performance results have certain limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not been executed, the results may have under-or-over compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown.” [This boilerplate statement indicates that the strategies/models offered may have material snooping bias (Chapter 3) and may not adequately disclose or account for investment frictions (Chapter 4).]

“Performance reflects gross profit or loss and is exclusive of commissions, trading fees and subscription costs.” [Such a statement more explicitly suggests that net profitability may be unattractive.]

“You should always check with your licensed financial advisor and tax advisor to determine the suitability of any investment.” [While seemingly telling investors that they are incapable of making good decisions on their own, the intent of such statements may be to emphasize that the offeror is not accountable for the usefulness of offered services.]

The legal disclaimers are good reminders not to take the marketing statements and supporting data at face value.

Another step investors can take to screen investment experts is to check how supporting data for past performance claims (backtests or stream of returns) addresses issues raised in Chapters 2 through 6, such as:

- Is the sample period long compared to both indicator and return measurement intervals (Chapter 1)? For example, if the strategy employs a 10-month moving average as an input, the sample should span many 10-month intervals.

- Are the assumptions underlying a backtest logically sequenced for realistic implementation (Chapter 2)? An example of an unrealistic assumption is a “possible” return stream for a trading strategy based on exits at price peaks knowable only in retrospect. Another example is setting an indicator parameter value based on knowledge of its full-sample behavior and then using that value within the sample.

- Are parameter values of key indicators optimized (snooped, per Chapter 3), such that they are unlikely to perform as well in a future period? While the optimal values are probably the best values to use, out-of-sample performance is likely to be lower than backtested performance.

- Does past performance commence with a strong initial burst (perhaps based on backtesting) and then substantially drop off. Such a scenario suggests the expert picked a lucky start date within a backtest period (snooped test periods, per Chapter 3).

- Does outperformance concentrate in a short interval during the sample period, suggesting lucky circumstances? For example, does a strategy perform very well during the 2008 market crash, but not before or after?

- If the expert manages multiple services, are they all outperforming, or just the one being promoted? The latter case suggests strategy snooping (Chapter 3) .

- What are the assumptions about investment frictions (Chapter 4)? Strategies that involve frequent trading, options and small positions are sensitive to frictions. If the cost of the service itself is high, it is especially important to account for it (whether by amortization across trades or by periodic portfolio-level debit).

- Does the performance of the strategy fade gradually over time? If so, the market may be adapting via its widespread use (Chapter 5).

- Are the returns claimed for a multi-position trading strategy clearly tied to an amount of capital required to implement them, or are capital requirements hazy (Chapter 6)? If trading opportunities cluster (feast or famine) or accumulate pending exit signals (bow wave), portfolio performance may be unattractive even when per-trade statistics seem attractive.

If answers to the above questions are not clear, it is prudent to ask the offeror to clarify.

In screening experts, it is also prudent for investors to ask (themselves, at least) how claims made in an offering square with evidence about the general level of financial market efficiency, and with human nature. Specifically:

- Is there convincing, corroborating research that supports the existence of reliable returns of the magnitude claimed for the type of strategy offered? Is there credible research that supports the existence of reliable returns of the magnitude claimed for any investing strategy? In other words, does it seem too good to be true? As discussed in Chapter 5, the level of competition for investment returns is fierce.

- Why have market makers, hedge fund managers or other sophisticated investors not discovered and extinguished the claimed market opportunity? Again (Chapter 5), it is imprudent to assume that trading counterparties are stupid.

- If an expert can reliably generate very large returns, why would this individual bother to sell the secret and administer an “educational” or advisory service rather than more directly and quickly get rich by exploiting the secret directly?

9.3 Summary

Key messages from this chapter are:

- Investment expertise is rare rather than common.

- Due diligence in screening potential investment experts is essentially stress testing their representations and involves a fair amount of work.

- Charlatans posing as investment experts should make it as difficult as possible to distinguish luck from skill, gross from net and trade-level from portfolio-level in their representations.