Each year, Forbes calculates the performance of columnist recommendations assuming: (1) equal initial investments in each stock pick when published; (2) 1% trading friction for each purchase; and, (3) matching benchmark investments in the S&P 500 Index for each pick with no trading friction. Because matching benchmark investments are spread across the year, the benchmark performance is not the same as the annual performance of the S&P 500 Index. In his February 10, 2016 column for Forbes, Ken Fisher reports the performance of the recommendations he made in his column during 2014, as follows: “Calculated by Forbes, taking a hypothetical 1% brokerage commission haircut, my basket lagged the S&P 500 (without any brokerage haircut) by 5% equal dollars invested. This is the seventh year out of 20 that my picks have lagged and the third year in a row.” Using data from the 18 annual performance summary columns covering 1998 through 2015, we find that:

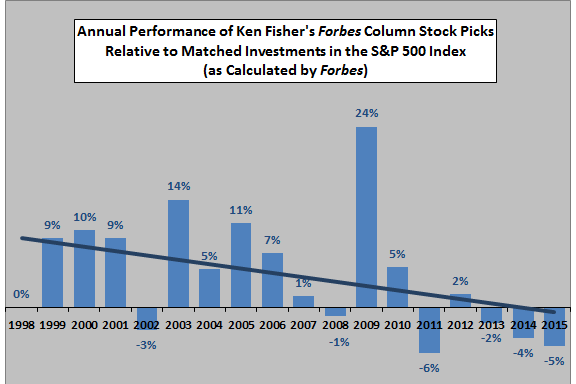

The following chart summarizes the annual performance of Ken Fisher’s public stock picks relative to matching investments in the S&P 500 Index, as calculated by Forbes, during 1998 through 2015. Ken Fisher’s public picks outperform matching S&P 500 Index investments in 11 of 18 years. On average, he outperforms matching benchmark investments by 4.2% per year. A linear best-fit trend line suggests that outperformance is fading over time, but the sample period is short for trend analysis given the variability of inputs.

Note that the S&P 500 Index may not be the most appropriate benchmark for Ken Fisher’s stock picks, many of which are non-U.S. companies.

Following are the essential descriptions of Ken Fisher’s annual stock picking performance by year (in reverse chronology) as reported in Forbes:

2015: “Calculated by Forbes, taking a hypothetical 1% brokerage commission haircut, my basket lagged the S&P 500 (without any brokerage haircut) by 5% equal dollars invested. This is the seventh year out of 20 that my picks have lagged and the third year in a row.”

2014: “My 55 2014 stock picks lagged badly. Equal money invested in each, upon publication, less a 1% commission haircut, did four percentage points worse than the same money plunked into the S&P 500 (with no haircut).”

2013: “FORBES’ statheads calculate that equal bucks bet on each stock pick from my twelve 2013 columns…would have done 2% worse than if put in the S&P 500 at the same times…”

2012: “For 2012 my picks would have done 1.7 percentage points better by year-end than the same amounts put into the S&P 500…”

2011: “Equal amounts invested in each of my 2011 stocks would have caused you a 6% loss. The same money put into the S&P 500 would have broken even.”

2010: “Had you put equal dollar amounts into each of my 72 recommendations for 2010 and subtracted a generous 1% for commissions, your total return would have been 18%, versus 12.8% for a similar investment in the S&P 500.”

2009: “During 2009 I made 65 recommendations (including six repeats). If you had put an equal sum into each you would be up 44.4%. If you had put the same money on the same dates into the S&P 500 you would have gained only 20.9%. The Forbes statistics department…docked my picks a 1% trading cost but didn’t dock the index. Neither return figure includes dividends, which are about one percentage point higher on my stocks.”

2008: “How were my results last year? In line with the market’s–which is to say, not good. …During 2008 I recommended 57 stocks. Equal money in each of my picks when first published less a 1% haircut for transaction costs would have lagged equal amounts in the S&P 500 by 1.1 percentage points (without a commission haircut).”

2007: “If you had bought all 60 of my 2007 recommendations you would be up 0.9% right now, assuming you lost 1% to transaction costs. Similarly timed investments in the S&P (without a transaction penalty) would be down a collective 0.5%.”

2006: “For 2006 I recommended 54 stocks, one more than in 2005, and my picks returned 15.7%, versus 8.7% for the S&P 500 tracker, an eerily similar seven-point spread.”

2005: “I suggested 53 stocks in 2005, including stocks re-recommended from 2004, and they collectively were up 14.3%, after a hypothetical 1% transaction haircut on new positions. Equal amounts invested in the S&P 500 (without haircut) at the same times were up only 3.4%. (In my column I choose not to write about companies I already hold in managed accounts.)”

2004: “In 2004 I made 51 recommendations. Had you put $10,000 into each, your $510,000 would have grown to a bit more than $574,000 by year-end, a 12.6% appreciation. This calculation assumes, moreover, a 1% haircut for transaction costs. Had you put the same money on the same dates into the S&P 500 (and with no haircut), your ending value would have been only $548,000. In other words, I was a good five points ahead of the market.”

2003: “Forbes’ statisticians assume that you lose 1% to commissions and bid/ask spreads on your recommended trades and compare the result with the performance of a commission-free investment on the same date in the S&P 500. By this measure my picks beat the market on average by 14%. This formula is too kind to my results last year, since I am trying to beat a global index. Last year the Morgan Stanley World Index did 5% better than the S&P 500, so I was beating my own target by only 9%.”

2002: “My picks declined an average 6% by year-end and would have left you 3% poorer than a hypothetical investor putting the same money at the same dates into a no-load [S&P 500 index] index fund. Actually, all of this is better than my firm’s individual clients fared. Note that the performance measure Forbes uses assumes that an investor loses 1% to commissions and bid/ask spreads on each round-trip trade for my stock picks. The hypothetical S&P 500 index fund against which the stock recommendations are compared has no trading costs and no overhead. My four short recommendations were better. They declined on average 23%, 20% more than the average decline of the S&P 500 from the same dates.”

2001: “At the outset, before the pros’ forecasts were in, I recommended three drug stocks: Schering, Akzo Nobel and Novo-Nordisk. Had you invested $10,000 in each of these, you would have lost 2.5% in 2001, factoring in a hypothetical 1% trading cost, or $750 on your $30,000 investment. You would have soundly beaten the market: Putting the $30,000 into the S&P would have lost you $3,420. Once I could do my own forecast, I advised staying out of equities, going for cash and bonds instead. This would have earned you around 4%. Not bad for a bad year.”

2000: “On my individual stock picks: Forbes accounts for them as if you invested equally in each selection when it appeared, less a 1% phantom brokerage cost, then compares the result with investing in an S&P 500 index on the same dates, in the same amounts. In 2000 this column broke even, beating the S&P by 10%, almost the same margin as in 1999. The column was lucky. My firm’s managed accounts didn’t beat the S&P 500 by anything like that.”

1999: “Let’s turn to my individual stock picks. Forbes calculates them each year as if you had invested equally in each of my stock selections, less a 1% phantom brokerage cost, and compares that with investing in [the S&P 500] index on the same dates, same amounts. In 1999 I beat the S&P 500 by 9%.”

1998: “If you had bought every one of this column’s recommendations last year, you would have done just as well as if you put your money, on the same dates, into the S&P 500 index — no better, no worse. That’s after docking all my recommendations, but not your hypothetical index investment, for a 1% commission cost.”

In summary, as calculated by Forbes, Ken Fisher’s public stock picks outperform the broad U.S. stock market over the past 18 years by an average 4.2% annually, but outperformance may be fading.

Cautions regarding findings include:

- We have not independently validated Forbes’ calculations. CXO Advisory Group LLC has no affiliation with Forbes.

- As noted, a sample of 18 years is small for annual performance measurement. Removing the best (worst) year of relative performance decreases (increases) average annual outperformance to 3.1% (4.8%).

- A representative of Fisher Investments states: “This does not represent the performance of Fisher Investments. It represents the short-term performance of stock picks from Ken Fisher’s Forbes Portfolio Strategy columns, which ran between 1984-2016. Ken’s stock picks in Forbes were restricted from Fisher Investments’ portfolio holdings at the time.”