Mebane Faber states in the first chapter of his 2016 book Invest with the House: Hacking the Top Hedge Funds: “We make two assumptions…: 1. There are active managers that can beat the market… 2. Superior active managers can be identified. …There is a general feeling that the market can’t be beat, and it is tough to get past that belief. A big challenge is separating luck from skill. But would anyone deny that some people are better than others at stock picking? Just like any other profession, the investment field has top experts who are paid handsomely for what they do. …You have access to the stock picks made by fund managers who often spend millions of dollars and every waking moment thinking and obsessing about the financial markets. …The best ones know everything there is to know about a company before they invest. …You can then build a stable of these managers and use them…for stock ideas to research and possibly implement in your own portfolio.” Based on prior research/experience and performances of the top ten (long) holdings from quarterly Form 13F filings for selected fund managers during January 2000 through December 2014, he concludes that:

From Chapter 2, “Berkshire Hathaway, Warren Buffett, and Charlie Munger” (Pages 20, 22-23): “The SEC maintains these filings on its EDGAR database and posts the electronic versions of 13F filings within a day of receiving the filings. Other websites, including EDGAR Online, Bloomberg, and FactSet/LionShares, aggregate the information into more usable and searchable formats, often for a fee. …The data is forty-five-days ‘stale’ when you see it, and the manager may very well not even own a particular stock by the time the 13F is posted. In addition, he may have added a stock at the start of the ninety-day reporting cycle, so a ‘new’ stock could have been purchased as long as 135 days ago. To further muddy the waters, some managers game the system by omitting certain recently acquired holdings and then filing amended 13F forms later. But even with all those delays, there is plenty of rich data here that you can use. By sticking with managers who have long holding periods, the delay in reporting times should not be a major factor in your own performance if you try to piggyback. …The portfolios I will track are long only. Most hedge funds also short and/or use derivatives to hedge or leverage their ideas. But these positions do not show up on the 13F filing, so they will not concern us here.”

From Chapter 3, “The Good and Bad About a 13F Strategy” (Pages 38-39): “We are now going to take a look at over twenty of my favorite managers to track for new ideas. There was no specific screening requirements to arrive at these funds; rather it is a combination of years of study coupled with quantitative as well as subjective analysis. Another fifteen fund profiles are included in the Appendix that have shorter investment track records. I will offer a very brief introduction to each manager as well as his or her backtested performance to 2000 and current holdings as of the most recent 13F filing on November 15, 2015.”

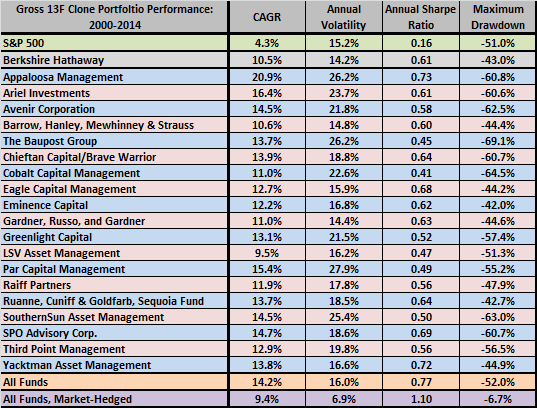

From Chapters 2, 4-24: The following table summarizes gross performance statistics for clone portfolios constructed and maintained as described above, including compound annual growth rate (CAGR), annual volatility, annual Sharpe ratio and maximum drawdown. The “All Funds” line combines holdings, including Berkshire Hathaway (and is therefore a 200-stock portfolio). The “All Funds, Market-Hedged” line additionally shorts the S&P 500 Index via futures to maintain market neutrality.

From Chapter 23, “Fund Groups and Strategies” (Pages 149, 151, 154): “…an investor can create a hedge fund of funds by combining a number of funds into one portfolio. The investor could simply take the top ten holdings from each fund and update the portfolio in the same method as before. This option gives the investor the additional benefit of diversifying his or her risk across multiple managers. …A more robust method would be to combine a number of managers whose methodologies differ substantially… …Another application of fund groups is applying a consensus approach to a portfolio. This tactic involves purchasing the stocks that are held by more than one fund manager.”

From Chapter 24, “Hedging” (Page 167): “Investors could employ a simple hedging strategy, buying puts or shorting various indices with futures to reduce volatility and market exposure.”

From Chapter 26, “Implementation” (Page 171): “…it is very important to pay attention to commissions and spreads that an investor would pay to execute this portfolio.”

In summary, investors will likely find Invest with the House an accessible approach to extracting, with a lag, any alphas in the long sides of many hedge funds or combinations thereof via Form 13F filings.

Cautions regarding conclusions include:

- Performance statistics are gross, not net. Accounting for data acquisition costs and trading frictions for quarterly rebalancing of clone portfolios (and costs of maintaining a 100% hedge per Chapter 24) would lower returns. Delegating these tasks to a fund manager would involve administrative/management fees.

- The 15-year sample period is not long for analysis of annual performance and may be sensitive to the sample start date. The sample may over-represent the effect of bear markets (two deep bear markets in 15 years).