Do individual investors exhibit good or bad timing in stock transactions of recent years? In the August 2015 version of their paper entitled “Fool’s Mate: What Does CHESS [Clearing House Electronic Subregister System] Tell Us About Individual Investor Trading Performance?”, Reza Bradrania, Andrew Grant, Joakim Westerholm and Wei Wu examine the short-term performance of stocks with unusual buying or selling pressure among individual Australian investors, Australian institutions or non-Australian (foreign) institutions. They define unusual pressure as the fifths (quintiles) of stocks with the most extreme buy/sell imbalances. Using daily closing stock holdings (capturing positions held at least overnight) aggregated by investor category and price/volume data for each of 2,841 Australian stocks during January 2009 through mid-August 2014, they find that:

- Over the sample period:

- The average weekly return of small (large) stocks is 0.654% (0.025%), with average standard deviation of weekly returns 10.0% (3.08%).

- On average, foreign institutions hold 58.5% of the Australian market, followed by domestic institutions (27.8%) and individuals (13.6%). Individuals hold on average 18.6% (7.45%) of small (large) stock capitalization. Foreigners account for most of the growth in market value.

- Individuals tend to be trend followers (contrarians) when they buy or sell small (large/medium) stocks.

- With respect to trade timing of individual investors:

- The quintile of stocks with the lowest daily buying pressure among individuals underperforms the quintile with the highest by an average 0.93%, 0.67% and 0.12% during the next one, two and three days, respectively.

- Outperformance derives from both sells and buys. The quintile of stocks with the lowest (highest) daily net buying pressure among individuals generates an average market-adjusted return of +0.47% (-0.46%) the next day.

- Abnormal performance only partially reverses at a 20-day horizon.

- Abnormal performance is more pronounced among small stocks.

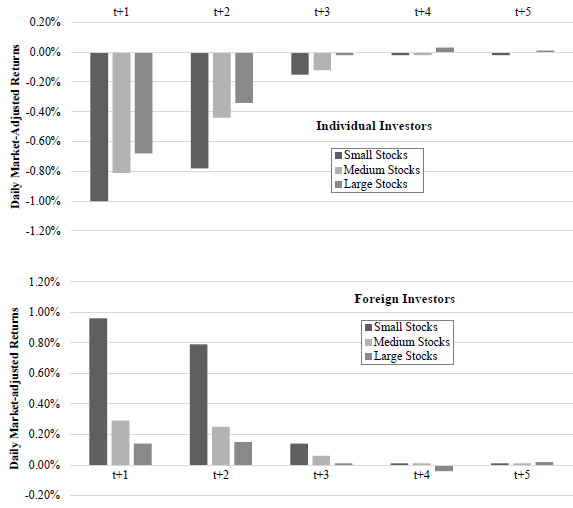

- The main beneficiaries of poor individual trade timing are foreign institutions (see the charts below). Results suggest that individuals (foreign institutions) take (provide) liquidity.

- Results are generally robust for 2009-2011 and 2012-2014 subperiods, but are weaker for the latter.

The following charts, taken from the paper, summarize trade timing performance of individual Australian investors and non-Australian institutional investors over the sample period. The upper chart presents average market-adjusted returns over the next five days for portfolios that are each day long (short) the equally weighted Australian stocks with the strongest (weakest) buying pressure among individuals. The lower chart presents average market-adjusted returns over the next five days for portfolios that are each day long (short) the equally weighted Australian stocks with the strongest (weakest) buying pressure among foreign institutions.

Results suggest that individuals require liquidity and pay a premium for it, while foreign institutions offer liquidity and earn a premium for it.

In summary, evidence indicates that individual Australian investors time stock trades poorly on average, thereby transferring wealth to non-Australian institutional traders.

Cautions regarding findings include:

- Reported returns are gross, not net. Accounting for trading frictions would lower these returns (more for individuals than institutions).

- For the long-short portfolio returns, shorting costs would further lower returns. Shorting may not be feasible for some stocks.

- The data used are likely not available for real-time exploitation of individual investor buying pressure.

- Findings may differ across markets.