Are illiquid assets competitive as investments with liquid financial assets over the long run? In his March 2016 paper entitled “The Long-Term Returns to Durable Assets”, Christophe Spaenjers summarizes long-term returns for three types of illiquid assets since the start of the 20th century:

- Houses and farmland.

- Collectibles (art, stamps, wine and violins).

- Gold, silver and diamonds.

He focuses on capital gains but comments on ancillary costs and potential associated income where relevant. Using available monthly price indexes for these assets from a variety of sources during 1900 through 2014, he finds that:

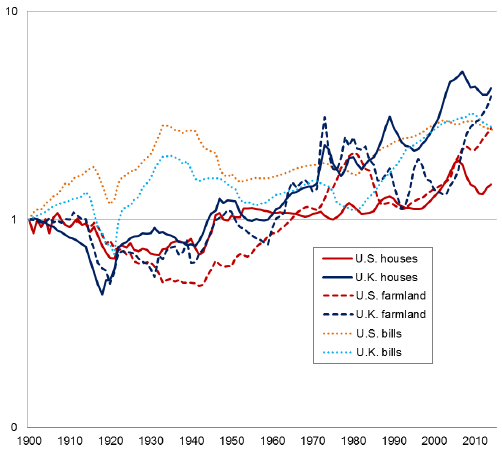

- Regarding houses and farmland:

- Gross long-run returns are low, comparable to those for government bills (see the first chart below).

- Early in the sample period, they lose real value.

- Rental income can substantially boost returns.

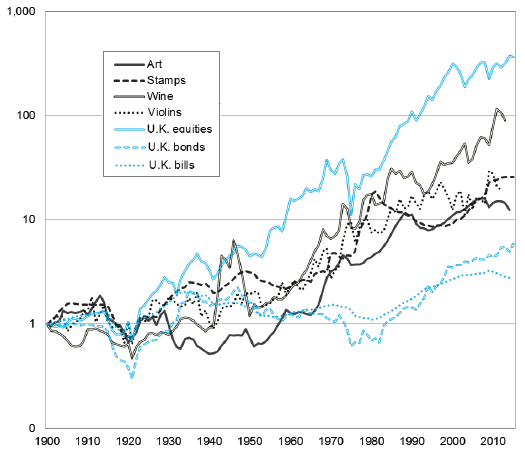

- Regarding collectibles (see the second chart below):

- Based on gross long-run data, they outperform government bonds but underperform equities.

- Returns are volatile and transaction costs very high (easily exceeding 25%).

- Good performance generally concentrates in the last half-century.

- Monthly pairwise correlations among collectible categories are relatively low, all below 0.22.

- Only the wine index accounts for storage and insurance costs.

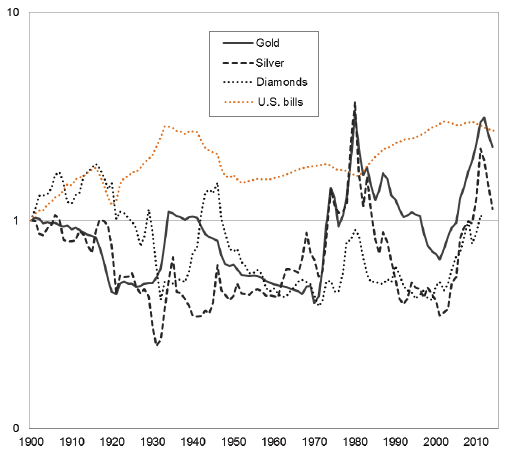

- Regarding gold, silver and diamonds (see the third chart below):

- Gross long-run returns are low and volatile, mostly underperforming government bills.

- Gold is more volatile than equities since the end of price constraints in 1975.

- None of the illiquid assets are good inflation hedges, but they may have some value for diversification of stocks and bonds.

The following chart, taken from the paper, tracks on a logarithmic scale real gross price indexes for houses and farmland in the U.S. and UK. Indexes do not account for any rental income, property taxes, costs of upkeep or tax benefits. Results suggest a long-run performance comparable to government bills.

The next chart, also from the paper, tracks on a logarithmic scale real gross price indexes for four categories of collectibles in British pounds. Except for wine, indexes do not account for storage and insurance costs. Results suggest a long-run performance greater than government bonds but less than equities. However, transactions costs for collectibles are very high.

The final chart, also from the paper, tracks on a logarithmic scale real gross price indexes for gold, silver and diamonds in U.S. dollars. Indexes do not account for storage and insurance costs. Results suggest a long-run performance inferior to that of government bills. Gold pricing is constrained for part of the sample period.

In summary, evidence suggests that any value of illiquid assets in portfolio enhancement would derive not from high returns but rather from diversification of stocks and bonds.

Cautions regarding findings include:

- The paper does not explicitly test the portfolio diversification power of illiquid assets.

- As noted in the paper, price series construction methods sometimes differ from those conventionally used in financial markets.

- Except for wine, the indexes used in the paper do not account for costs of holding/maintaining physical assets, nor do they account for any ancillary benefit of rental income for real estate.

- As noted in the paper, transaction costs are very high for some illiquid assets.