Is there a way to avoid the stock momentum crashes that occur when the positive feedback loop between past and future returns breaks down? In his November 2013 paper entitled “Crowded Trades, Short Covering, and Momentum Crashes“, Philip Yan investigates the power of the interaction between short interest and institutional trading activity to explain stock momentum crashes and thereby offer a way to avoid these crashes. Each month he sorts stocks into ranked tenths (deciles) based on returns from 12 months ago to one month ago (skipping the most recent month to avoid reversals). He reforms each month baseline winner and loser portfolios from the value-weighted deciles of extreme high and low returns, respectively. He then segments the loser portfolio into crowded losers (stocks that are most shorted and have the highest institutional exit rate) and non-crowded losers (stocks that are most shorted but do not have the highest institutional exit rate). The most shorted losers are those within the fifth of stocks with the highest short interest ratios (short interest divided by shares outstanding). The losers with the highest institutional exit rates are those within the fifth of stocks with the most shares completely liquidated by institutional investors divided by shares outstanding. He defines three value-weighted long-short portfolios: (1) the baseline portfolio buys the baseline winners and shorts the baseline losers; (2) the crowded portfolio buys the baseline winners and shorts the crowded losers; and, (3) the non-crowded portfolio buys the baseline winners and shorts the non-crowded losers. Using daily and monthly stock return, monthly short interest and quarterly institutional ownership data during January 1980 through September 2012, high-frequency short sales data during 2005 through 2012, and monthly price data for 63 futures contract series as available during January 1980 through June 2013, he finds that:

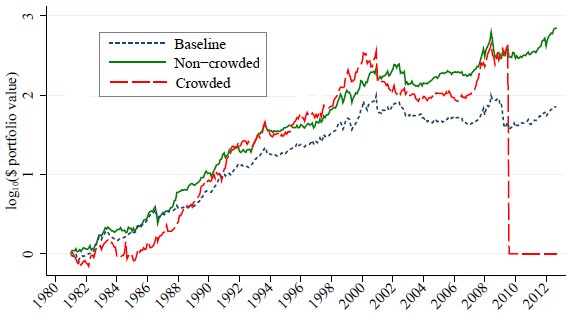

- Whether precisely hedged for market exposure or not, the non-crowded portfolio generally outperforms the crowded portfolio, with much less drawdown (crash) exposure. The non-crowded portfolio also outperforms the baseline portfolio. Specifically, the gross annualized average returns, Sharpe ratios and return-to-drawdown ratios for the simple long-short portfolios are, respectively (see the chart below):

- 12.6%, 0.48 and 0.67 for the baseline portfolio.

- 22.1%, 0.72 and 1.28 for the non-crowded portfolio.

- 16.4%, 0.37 and 0.55 for the crowded portfolio.

- High-frequency short sales data indicate that short covering is especially severe in the crowded loser portfolio during momentum crashes.

- A futures momentum strategy with market exposure correctly hedged does not have crashes and exhibits a return-to-drawdown ratio 50% higher than that for stocks, suggesting that stock momentum crashes are a by-product of shorting constraints.

The following chart, taken from the paper, tracks gross log cumulative returns of $1 initial investments in the baseline, non-crowded and crowded long-short stock momentum strategies as defined above over the sample period. The non-crowded strategy (with losers having high short interest ratios but not strong institutional exits) outperforms both the crowded and baseline strategies by boosting return and avoiding crashes.

In summary, evidence indicates that investors pursuing stock momentum strategies may be able to boost performance by excluding stocks with both high short interest ratios and evidence of abandonment by institutions.

Cautions regarding findings include:

- Reported performance data are gross, not net. Accounting for trading frictions, which tend to be high for monthly momentum strategies due to high turnover, would dampen performance. Including shorting costs would further lower performance.

- Frictions/costs may vary systematically between baseline and highly shorted stocks and between crowded and non-crowded stocks, such that net findings would differ from gross findings. Shorting may not be feasible for some stocks, especially crowded losers. (See “Lendable Share Supply a Roadblock to Shorting Strategies?”.)

- Many investors may not be able to hold enough individual stocks to assure outcome reliability.

- There may be data snooping bias in strategy parameter settings.