Can an approach that describes each asset class as a bundle of sensitivities to economic/market conditions improve investment decision-making? In their March 2016 paper entitled “Factor-Based Investing”, Pim Lausberg, Alfred Slager and Philip Stork develop a “heat map” to summarize how returns for seven asset classes relate to six economic/market factors. The seven asset classes are: (1) government bonds; (2) investment grade corporate bonds; (3) high-yield corporate bonds; (4) global equity; (5) real estate; (6) commodities; and, (7) hedge funds. The six economic/market factors are: (1) change in consensus forecast of next-year economic growth; (2) change in consensus forecast for next-year inflation; (3) illiquidity (Bloomberg market liquidity indexes); (4) volatility of stock market indexes; (5) credit spread (return on investment grade corporate bonds minus return on duration-matched U.S. Treasuries); and, (6) term spread (return on government bonds of duration 7-10 years minus return on government bills of duration three months). They also provide suggestions on how to use the heat map in the investment process. Using monthly asset class returns and factor estimation inputs during 1996 through 2013, they find that:

- Asset prices react significantly to economic news and market regime changes, such that economic/market factors explain most of contemporaneous variations in asset class returns.

- However, there is little agreement in the body of research on whether economic/market factors predict asset class returns.

- The primary value of the heat map summarizing asset class return-factor relationships is an understanding of asset class allocation risk across economic/market conditions.

- Investors who have beliefs about economic/market trends can use the heat map also for tactical asset class allocation tilts to exploit the trends.

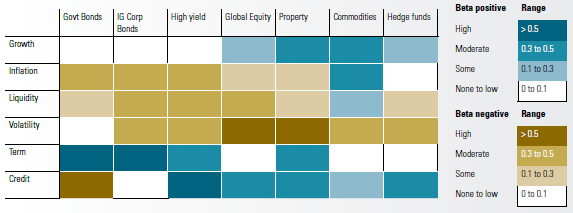

The following chart, taken from the paper, is the color-coded heat map summarizing relationships between asset class returns (across the top) and economic/market conditions (top to bottom on the left). Positive (negative) betas indicate that returns and factor values tend to move in the same (opposite) directions. Beta magnitude indicates strength of relationship. This visualization can help investors construct allocations that balance risks across economic/market conditions.

In summary, investors may be able to use the asset class-factor relationship heat map to construct a portfolio resistant to deep losses during any particular economic/market state.

Cautions regarding findings include:

- The sample period is one of secular decline in inflation and interest rates (bond bull market). Findings may be different for a sample containing an extended bond bear market. In other words, the heat map may not be stable over other samples.

- Heat map development relies on gross returns to asset class indexes. Accounting for the costs of translating indexes into liquid funds, which may vary by asset class, may alter findings.

- The selected sample period/factors may inherit snooping bias from prior research, such that confidence in reported return-factor betas is overstated.