Are winning (losing) stocks with the strongest upward (downward) acceleration the best bets for a momentum strategy? In their July 2013 paper entitled “Investor Attention, Visual Price Pattern, and Momentum Investing”, Li-Wen Chen and Hsin-Yi Yu investigate whether visually striking patterns of past prices tend to grab investor attention, induce overreaction and amplify the momentum effect. They first rank stocks into fifths (quintiles) based on past returns to identify winners and losers (with a skip-month between the ranking interval and portfolio formation to avoid reversals). They then regress daily returns of winners and losers versus time squared over the past 12 months, with a positive (negative) coefficient indicating a convex (concave) price trajectory curvature, and further sort winner and loser quintiles into fifths based on curvature. Intuitively, winners (losers) with convex, upward accelerating (concave, downward accelerating) price trajectories most strongly attract trader attention and most reliably exhibit price momentum. They test this intuition by each month forming nine momentum hedge portfolios that are:

- Long winners and short losers (traditional momentum approach).

- Long winners and short convex-shaped (decelerating) losers.

- Long winners and short concave-shaped (accelerating) losers.

- Long concave-shaped (decelerating) winners and short losers.

- Long convex-shaped (accelerating) winners and short losers.

- Long convex-shaped (accelerating) winners and short concave-shaped (accelerating) losers.

- Long concave-shaped (decelerating) winners and short convex-shaped (decelerating) losers.

- Long convex-shaped (accelerating) winners and short convex-shaped (decelerating) losers.

- Long concave-shaped (decelerating) winners and short (accelerating) concave-shaped losers.

Portfolios are equally weighted with baseline settings of a 12-month momentum ranking interval and a six-month holding interval (six overlapping portfolios in any month). Using monthly and daily prices and accounting data for a broad sample of U.S. common stocks, along with contemporaneous return factors and economic data, during January 1962 through December 2011, they find that:

- Gross returns and three-factor (market, size, book-to-market ratio) alphas of convex winners (concave losers) are significantly higher (lower) than those for concave winners (convex losers). Findings are generally robust for subperiods, different stock exchanges, exclusion of January returns and most ranking and holding intervals. For the baseline 12-month ranking and six-month holding intervals (see the chart below):

- Over the entire sample period, the basic momentum effect (strategy 1) generates an average gross monthly return of 0.83%. The intuitively most (least) attractive of the above alternatives is strategy 6 (7), which generates an average gross monthly return of 1.32% (0.47%).

- Corresponding gross monthly three-factor alphas for strategies 1, 6 and 7 are 1.23%, 1.75% and 0.87%.

- Strategy 6 (7) outperforms (underperforms) in all subperiods. During the last two decades, strategy 6 generates an average gross monthly return of 0.98%, while none of the other strategies are significantly profitable.

- Reducing the ranking interval generally suppresses the difference in gross returns between strategies 1 and 6. When the ranking interval is less than three months, the difference is insignificant, suggesting that traders cannot visualize a pattern.

- In general, strategies peak in profitability soon after portfolio formation, and exhibit reversals for a holding intervals of 36 months or longer.

- Removing the skip-month between ranking and holding intervals improves momentum returns, especially when the ranking interval is long and the holding period is short.

- All nine strategies exhibit significant gross profitability only during economic expansions. Strategy 6, for example, generates an average gross monthly return of 1.55% (0.49%) during economic expansions (contractions).

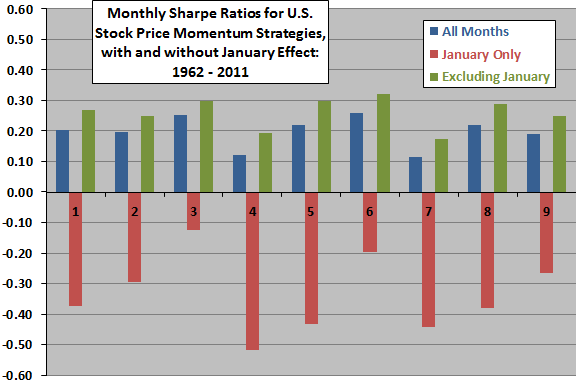

The following chart, constructed from data in the paper, shows Sharpe ratios for all nine momentum hedge portfolios listed above for the baseline 12-month ranking interval and six-month holding interval over the entire sample period. Results indicate that:

- Focusing on winners with convex price trajectories and/or losers with concave price trajectories boosts the performance of a traditional momentum portfolio. Ignoring winners with concave price trajectories appears to be key.

- January is consistently a bad month for stock momentum strategies, whether enhanced with an acceleration filter or not.

In summary, evidence indicates that investors can boost gross returns for a stock price momentum strategy by focusing on winners with convex price patterns (accelerating upward) and losers with concave price patterns (accelerating downward).

Cautions regarding findings include:

- Reported returns are gross, not net. The testing approach of overlapping portfolios involves many positions (high aggregate transaction costs). Accounting for trading frictions would reduce these returns.

- The study does not examine the feasibility and cost of shorting specified losers.

- Testing many strategies and parameter variations (convex-concave curvature alternatives, ranking intervals and holding periods) on the same dataset introduces data snooping bias, such that the best-performing strategy incorporates luck and therefore overstates out-of-sample expectations .