Can systematic, contrarian sports betting usefully diversify conventional investments? In their June 2016 paper entitled “Sports Betting As a New Asset Class: Can a Sports Trader Beat Hedge Fund Managers from 2010-2016?”, Lovjit Thukral and Pedro Vergel investigate whether a specific sports betting strategy outperforms and diversifies the Credit Suisse Hedge Fund Index and the S&P 500 Index. The strategy hypothesizes that horse racing favorites are consistently overrated by betting 1% of a hypothetical portfolio against the top four (lowest odds) horses in each regulated race in the UK. Using historical data from Betfair Exchange for 57,000 horse races and contemporaneous annual returns for the Credit Suisse Hedge Fund Index and the S&P 500 Total Return Index during January 2010 through early January 2016, they find that:

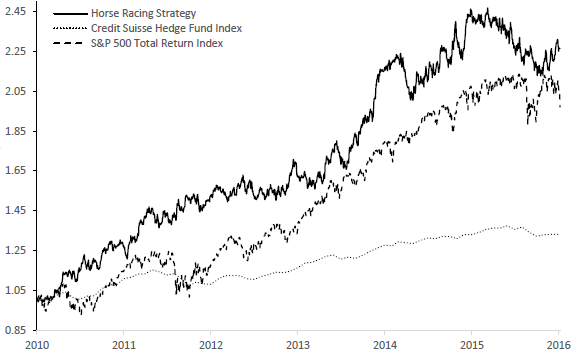

- The betting strategy is competitive with the Credit Suisse Hedge Fund Index and the S&P 500 Total Return Index based on gross cumulative performance (see the chart below) and gross annual Sharpe ratio (1.12, versus 1.11 and 0.69, respectively).

- Strategy returns are uncorrelated to those of hedge funds and the U.S. stock market.

The following chart, taken from the paper, tracks the normalized gross performances of the horse race betting strategy specified above, the Credit Suisse Hedge Fund Index and the S&P 500 Total Return Index over the sample period. The betting strategy generally outperforms, but does exhibit stock market-like volatility.

In summary, evidence suggests that systematically betting against horse racing favorites provides attractive gross returns, uncorrelated to those of hedge funds and U.S. equities.

Cautions regarding findings include:

- The sample period is very short for assessment of annual performance.

- As noted in the paper, the capacity of the specified strategy may be limited, with large bets or many small bets materially moving the odds.

- As noted in the paper, results are gross, not net. The authors state that: “…in our experience commissions are quite small and do not materially affect our returns.”

- Results may not apply to other sports betting due to either different levels of market efficiency or unavailability of contrarian bets.

- There may be snooping bias in specification of the top four horses, thereby overstating expectations.