Are there parallels at the country stock market level of the size, value and momentum effects observed for individual stocks? In their January 2014 paper entitled “Value, Size and Momentum across Countries”, Adam Zaremba and Przemysław Konieczka investigate country-level value, size and momentum premiums. They measure these factors at the country level as:

- Value (V): book-to-market ratio of country stocks aggregated via the weighting scheme used to construct the country stock index at the time of portfolio formation.

- Size (S): total market capitalization of country stocks at the time of portfolio formation.

- Long-Term Momentum (LTM): country index return during the 12 months before portfolio formation.

- Short-Term Momentum (STM): country index return during the month before portfolio formation.

They calculate these factors using either MSCI equity indexes (47 indexes available at the beginning of the sample period) or local stock indexes (only 24 indexes available at the beginning of the sample period). They measure the country-level premium for each factor as the return on an equally weighted portfolio that is each month long (short) the 30% of countries with the highest (lowest) expected returns for that factor. They fully collateralize short sides with reserves in the risk-free rate. They also calculate a total market return as the capitalization-weighted average return across all country markets. They perform calculations separately in U.S. dollars, euros and yen. Using monthly firm/stock data for listed stocks as available within 66 countries from the end of May 2000 through November 2013, and contemporaneous Fama-French model U.S. factors, they find that:

- Average gross monthly premiums are materially positive for the V, S and LTM factors, regardless of index definition or base currency. The average gross monthly premium for the STM factor is positive but insignificant.

- Fama-French U.S. value and size factors almost fully explain the country-level value factor and partly explain the country-level size factor, regardless of base currency. They do not explain country-level momentum.

- LTM is perhaps the most attractive country-level factor:

- LTM raw and market-adjusted factor premiums are stronger than those for S and V.

- High-LTM countries outperform low-LTM countries, and they do so with lower volatility.

- The LTM factor premium is more consistent than V and S premiums, both of which are negative for 2008-2013.

- Country-level V, S, LTM and STM factors tend to reinforce each other, such that double-sorts outperform single-sorts. Based on MSCI indexes in U.S. dollars (robust to alternatives), three combinations are particularly strong:

- LTM + V generates an average gross monthly return of 1.70% (22.6% annualized).

- LTM + S generates an average gross monthly return of 1.42% (18.6% annualized).

- STM + S generates an average gross monthly return of 1.14% (14.7% annualized).

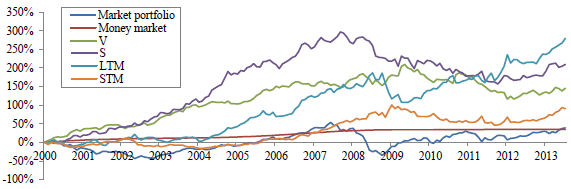

The following chart, taken from the paper, compares gross cumulative returns for the market portfolio, the risk-free rate (money market), and V, S, LTM and STM factor portfolios as constructed from local country indexes measured in U.S. dollars. Over the entire sample period, V, S and LTM substantially outperform the market on a gross basis, but STM does not. The LTM factor premium is more consistent than the V and S premiums, both of which are negative (downward trending) since 2008.

In summary, recent evidence suggests that value, size and momentum factors that partly explain variations in individual stock returns may also help explain variations in country stock market returns.

Cautions regarding findings include:

- Return calculations are gross, not net. Including the costs of monthly factor portfolio reformation would reduce reported returns. Different factors may generate different portfolio turnovers.

- Use of country indexes rather than tradable assets ignores the costs of maintaining liquid tracking funds. These costs may vary by country.

- Hedge portfolio calculations ignore costs/feasibility of shorting country indexes.

- The sample period, limited by data availability, is short for testing annual book value. It is also short in terms of variety of worldwide economic conditions.

- Testing of multiple factors/combinations of factors on the same set of data introduces data snooping bias, such that the best performing factor/combination tends to overstate expectations.

- Calculating value and size at the country level is infeasible for many investors (and costly if delegated).

See also the closely related “Stock Markets Have Value and Size, Too?”.