Is there an easy way to turn conventional stock momentum crashes into gains? In the March 2017 version of her paper entitled “Dynamic Momentum and Contrarian Trading”, Victoria Dobrynskaya examines the timing of momentum crashes and tests a simple dynamic strategy designed to turn the crashes into gains. This strategy follows a conventional stock momentum strategy most of the time, but flips to a contrarian strategy for three months after each market plunge with a lag of one month. The conventional momentum hedge portfolio is each month long the tenth (decile) or third (tercile), depending on sample breadth, of stocks with the highest cumulative returns from 12 months ago to one month ago and short the tenth or third with the lowest cumulative returns. The contrarian hedge portfolio flips the long and short positions. For her baseline case, she defines a market plunge as a monthly return more than 1.5 standard deviations of monthly returns below the average monthly market return (measured in-sample). For most analyses, she employs the Fama-French U.S. equal-weighted and value-weighted extreme decile momentum hedge portfolios during January 1927 through July 2015. For global developed market analyses, she employs extreme tercile momentum hedge portfolios from various sources during November 1990 through March 2016. She also considers long-only momentum portfolios for emerging markets: one broad during June 1991 through March 2016) and one narrow (Latin American only) during June 1995 through March 2016. Using this data, she finds that:

- For the long 1927-2015 U.S. sample:

- The conventional momentum hedge portfolio tends to perform poorly for 2-4 months after low market returns. In other words, momentum crashes tend to happen not during the month after a market plunge, but during the next 1-3 months.

- Dynamic momentum, holding a contrarian position during only 15% of months, turns all major conventional momentum crashes into gains. Specifically (see the chart below):

- Annualized average gross return for equal-weighted (value-weighted) dynamic momentum is 17.4% (18.4%), compared to 10.0% (14.6%) for conventional momentum and 11.2% for the market.

- Annualized volatility for equal-weighted (value-weighted) dynamic momentum is 26.3% (27.0%), compared to 26.7% (27.1%) for conventional momentum and 18.7% for the market.

- Annualized gross Sharpe ratio for equal-weighted (value-weighted) dynamic momentum is 0.66 (0.68), compared to 0.38 (0.54) for conventional momentum and 0.60 for the market.

- Market beta for equal-weighted (value-weighted) dynamic momentum is 0.44 (0.51), compared to -0.42 (-0.53) for conventional momentum.

- The deepest monthly loss for equal-weighted (value-weighted) dynamic momentum is -30.3% (-25.0%), compared to -89.7% (-77.0%) for conventional momentum.

- Outperformance of dynamic momentum compared to conventional momentum derives largely from taking long positions in past losers during rebounds from market crashes.

- Dynamic momentum performs well in all global regions in recent decades, even in Japan where conventional momentum does not work. Specifically:

- Average gross returns of dynamic momentum are about 1.5 times those of conventional momentum in all regions.

- Highest (lowest) gross returns occur in Europe and Asia-Pacific (Japan).

- Dynamic momentum generally has higher Sharpe ratios than conventional momentum, with positive but low local market betas.

- Regarding robustness tests on U.S. data:

- In-sample monthly market plunge thresholds of 2 and 2.5 standard deviations below the monthly average generate higher annualized average gross returns and higher annualized gross Sharpe ratios than does the 1.5 standard deviations threshold, but have worse worst months. A threshold of 1 standard deviation performs worse than 1.5. A threshold between 1.5 and 2 standard deviations seems balanced.

- Dynamic momentum is robust across three 30-year subperiods and during the last 15 years of the sample period. Over the last 15 years, dynamic momentum generates equal-weighted (value-weighted) annualized average gross return 21.8% (17.5%) with annualized gross Sharpe ratio 0.76 (0.52).

- Dynamic momentum does incur some trading frictions incremental to those of conventional momentum when long and short positions reverse during 4-7% of all months.

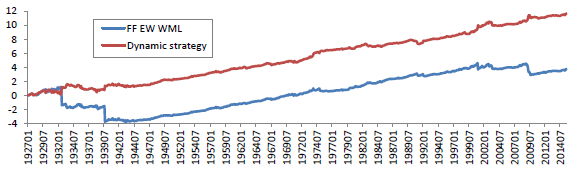

The following chart, taken from the paper, compares gross cumulative returns (natural logarithm) of conventional momentum (FF EW WML) and dynamic momentum (Dynamic strategy) for the long U.S. sample, with portfolios equally weighted. Results show that dynamic momentum avoids three major conventional momentum crashes.

In summary, evidence from in-sample tests suggests that investors may be able to avoid (and reverse) conventional stock momentum crashes by flipping to a contrarian stance during months two through four after a broad market monthly plunge.

Cautions regarding findings include:

- As noted, dynamic momentum tests are in-sample because the threshold for switching between momentum and contrarian positions derives from the full sample (confirmed by the author). Results for a test using only data available in real time to determine the threshold for switches may differ substantially.

- The in-sample Sharpe ratios of equal-weighted and value-weighted dynamic momentum are not much higher than that of the market, reflective of the relatively high volatility of dynamic momentum.

- As illustrated in the chart above, dynamic momentum outperformance depends on avoiding a few deep conventional momentum crashes. The sample of deep crashes is very small, undermining confidence that future crashes will be reliably like them.

- Performance data are gross, not net. Stock momentum portfolios typically have fairly high turnover and therefore material monthly reformation frictions that would reduce average returns and Sharpe ratios. These frictions likely vary by market.