In which country stock markets is technical analysis likely to work best? In the October 2014 version of her paper entitled “Technical Analysis: A Cross-Country Analysis”, Jiali Fang investigates three potential cross-country determinants of technical trading profitability:

- An individualism index, measuring the degree to which individuals integrate via cultural groups.

- Market development and integrity metrics, including stock market size, stock market age, transaction costs and measures of investor protection, anti-director rights, ownership concentration and insider trading.

- Information uncertainty metrics, including aggregate market turnover, volatility of cash flow growth rate and book-to-market ratio.

She considers 26 previously studied trading rules employing only past prices, classified as: variable moving average (VMA) rules, fixed-length moving average (FMA) rules and trading range break-out (TRB) rules. VMA rules are long (short) an index when a short-term moving average is above (below) a long-term moving average. FMA rules are similar to VMA rules, but hold a newly signaled position a fixed interval of 10 days. TRB rules generate buy (sell) signals when price rises above (falls below) the resistance (support) defined by prices over a specified past interval. Tests include both regressions and model strategies that are long (short) the market index as signaled and invest in the risk-free asset when there is no signal. Using cultural metrics, daily stock market index data and economic/financial variables for 50 countries during March 1994 through March 2014, she finds that:

- In general, technical trading rules exhibit mixed effectiveness across countries.

- For example, VMA, FMA and TRB rules based on a one-day short-term price and a 50-day long-term moving average generate significantly positive gross results in 36, 13 and 27 of 50 countries, respectively. However, results are significantly negative in a few cases.

- VMA rules generally outperform FMA and TRB rules. On average, VMA rules are effective on a gross basis in 27 of 50 countries, compared to 15 and 21 for FMA and TRB rules, respectively.

- Shorter measurement intervals generally outperform longer ones. For example, on average, rules employing a 50-day long-term moving average exhibit gross predictive power in 24 countries, compared to only 14 countries for a 200-day long-term moving average.

- Technical trading rules do not work in the U.S. market.

- Technical trading returns tend to be higher in countries that are less individualistic, markets that are less developed and markets that exhibit higher information uncertainty.

- Individualism has the strongest explanatory power, explaining cross-country effectiveness for 21 of 26 technical trading rules, compared to 16 and 14 for market development and information uncertainty, respectively.

- Technical trading rules work better during the 20 years preceding the main 1994-2014 sample (per available older data), confirming that technical trading tends to be less effective in developed markets.

- Technical trading returns are substantially higher during NBER contractions than expansions, but are robust to other macroeconomic factors.

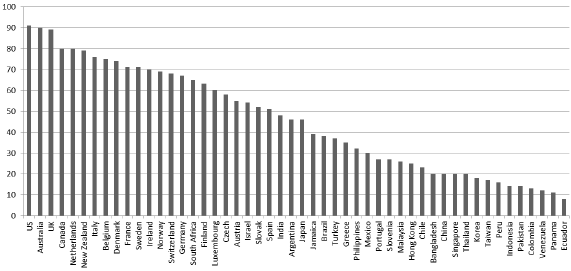

The following chart, taken from the paper, summarizes individualism indexes for the 50 countries examined in the study. In general, western countries such as the U.S., Australia, the UK, Canada and the Netherlands are more individualistic. Less develop and eastern countries such as Ecuador, Panama, Venezuela, Colombia and Pakistan are more collectivist. Japan, Argentina and India are mid-range. Individualism has the strongest explanatory power for the effectiveness of technical trading rules (low individualism indicates high effectiveness).

In summary, evidence suggests technical analysis still has practical value in country stock markets associated with collectivist cultures, undeveloped markets and high information uncertainty.

Cautions regarding findings include:

- Reported results are gross, not net. Including trading frictions for position changes and costs of shorting would reduce returns for technical trading rules. Shorting of country markets may not always be feasible. Since trading frictions vary considerably across countries, findings based on net returns may differ from those based on gross returns.

- As noted in the paper, the same technical trading rule can generate a strongly positive average gross return in one country market and a strongly negative average gross return in another.

- While the study does not actively snoop trading rules, there may be derivative snooping bias in the set or rules considered.