Does the market pay a premium to equity funds with relatively high “bad” (left tail) volatility? In their May 2013 paper entitled “Volatility vs. Tail Risk: Which One is Compensated in Equity Funds?”, James Xiong, Thomas Idzorek and Roger Ibbotson compare return premiums for conventional volatility (standard deviation of total returns) and tail risk (value-at-risk) across U.S. and non-U.S. equity mutual funds. Each month, they use the previous five years of monthly net total returns to sort funds into fifths (quintiles) based on volatility and on excess (relative to a normal distribution) value-at-risk for the worst 5% of returns. They estimate premiums for these two risk measures as the difference in average (arithmetic mean) returns between the riskiest and least risky quintiles in excess of the Treasury bill (T-bill) yield. Using monthly returns for the oldest share class for a broad sample of alive and dead open-end equity mutual funds (3,389 U.S. and 1,055 non-U.S.), and the contemporaneous T-bill yield, during January 1980 through September 2011, they find that:

- Volatility and value-at-risk measures have low correlations over the sample period for both U.S. and non-U.S. funds (-0.10 to 0.01, respectively), indicating that they capture different information about risk.

- Equity funds exhibit mixed results regarding a volatility premium:

- U.S. equity funds exhibit an annualized net volatility premium of 1.6% (volatile funds outperform). However, the most volatile quintile has the lowest net Sharpe ratio, and the geometric mean net returns for the least and most volatile quintiles are about equal.

- For non-U.S. equity funds, the annualized net volatility premium is -1.4%.

- Results based on fund beta instead of volatility are similar.

- Equity funds clearly exhibit a tail risk (excess value-at-risk) premium:

- Both U.S. and non-U.S. equity funds exhibit economically significant positive tail risk premiums (net annualized 2.7% and 2.5%, respectively), and these premiums persist after controlling for volatility.

- The corresponding four-factor (market, size, book-to-market, momentum) annualized net tail risk alphas are 2.6% and 2.9%, respectively, indicating that the tail risk premium is distinct from commonly used factor premiums.

- Results based on fund coskewness (skewness relative to market skewness) instead of value-at-risk as a measure of tail risk are similar but weaker.

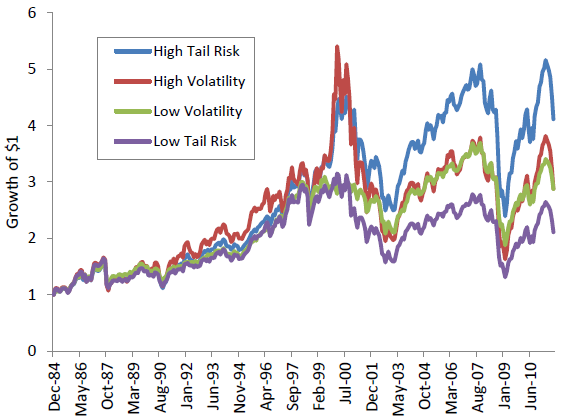

The following chart, taken from the paper, tracks cumulative values of $1.00 initial investments in the equally weighted extreme quintiles of U.S. equity funds sorted by lagged conventional volatility and separately by lagged excess value-at-risk (tail risk) over the sample period. High tail risk consistently beats low tail risk. However, high volatility does not consistently beat low volatility, such that extreme volatility quintiles have similar outcomes.

For non-U.S. equity funds (not shown), high tail risk consistently beats low tail risk, and low volatility consistently beats high volatility.

In summary, evidence mostly supports beliefs that investors: (1) earn no premium for assuming equity volatility risk; but, (2) do earn a premium for assuming equity tail risk.

Cautions regarding findings include:

- Findings are likely less reliable for realistic holdings of a few mutual funds.

- Among U.S. equity funds, results do not support avoiding volatility.