Is there a way to suppress the volatility and drawdowns of a mixed value and momentum stock strategy while retaining most of its benefit? In his September 2015 paper entitled “Learning to Play Offense and Defense: Combining Value and Momentum from the Bottom up, and the Top Down”, Mebane Faber examines the feasibility of a strategy that combines market valuation and market trend timing (defense) with a mixed value and momentum stock selection strategy (offense). Specifically:

For offense, he each month: (1) ranks stocks by each of price-to-earnings, price-to-book and earnings before interest and taxes-to-total enterprise value ratios and then re-ranks them by the average of the three separate value rankings; (2) ranks stocks by each of 3-month, 6-month and 12-month past returns and then re-ranks them by the average of the three separate momentum rankings; and, (3) forms an equally weighted portfolio of the top 100 value and top 100 momentum stocks and holds for three months (three overlapping portfolios).

For defense, he each month: (1) hedges half of the portfolio by shorting the S&P 500 Index if the long-term real earnings yield for the S&P 500 (inverse of the Cyclically Adjusted Price-Earnings ratio, CAPE or P/E10 as calculated by Robert Shiller, minus the most recently available actual 12-month U.S. inflation rate) is in the 20% of its lowest inception-to-date monthly values; and, (2) hedges half of the portfolio by shorting the S&P 500 Index if the index is below its 12-month simple moving average.

The overall portfolio can therefore be 100% long “offense” stocks, 50% hedged or market neutral. He does not account for costs of portfolio reformations or hedging. Using monthly total returns for all NYSE stocks in the top 60% of market capitalizations, monthly levels of the S&P 500 Total Return Index and monthly values of CAPE during 1964 through 2014, he finds that:

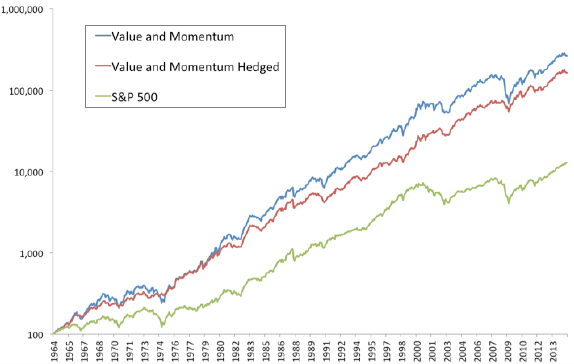

- The offense portfolio substantially outperforms the S&P 500 Total Return Index, with gross annualized return 16.7% (versus 10.0% for the index) and gross annual Sharpe ratio 0.62 (versus 0.33 for the index). However, the portfolio has higher annual volatility (18.7% versus 14.9%) and somewhat deeper maximum drawdown (-56% versus -51%).

- Adding defense to offense suppresses volatility (14.2%) but sacrifices some annualized return (15.6%), with gross annual Sharpe ratio 0.74. Adding defense substantially suppresses maximum drawdown (-27%). (See the chart below.)

- Results are generally robust to different market valuation and trend determination metrics for defense.

- As of September 2015, offense plus defense is market neutral, because the market is both overvalued and in a downtrend.

The following chart, taken from the paper, shows the trajectories on a logarithmic scale of the gross offense (Value and Momentum), gross offense plus defense (Value and Momentum Hedged) and the S&P 500 Total Return Index over the sample period.

In summary, evidence indicates that a portfolio of value and momentum stocks outperforms the broad market on a gross basis and that simple market valuation and trend rules suppress volatility/drawdown of such a portfolio.

Cautions regarding findings include:

- As noted in the paper, the analysis benefits from hindsight (knowing that the specified value and momentum metrics outperformed the market historically), thereby overstating expected returns.

- As noted in the paper, calculations ignore the trading frictions of portfolio maintenance, which would have been large over part of the sample period. Calculations also ignore any costs of shorting the S&P 500 Index as specified, which may not have been practical over the entire sample period.

- There is some lag in Shiller’s recent-month calculations of CAPE, such that the calculation for the most recent month is missing the last six months of earnings (in other words, it is based on 9.5 years of earnings data, lagged six months). There is therefore some look-ahead bias in the historical data. However, the author reports that findings are not sensitive to the lag.

- Few individuals can efficiently hold three overlapping portfolios of 200 stocks. Most would have to turn to a fund and pay associated fees or hold a much smaller, likely riskier portfolio.

- Timely data acquisition and processing may have been problematic/costly over much of the sample period.

Performance statistics for a long-only, estimated net version of the strategy are available via “Combining Value and Momentum in Stock Selection and Market Timing”.