When Equity Market Momentum Does and Does Not Work

July 10, 2026 - Equity Premium, Fundamental Valuation, Momentum Investing

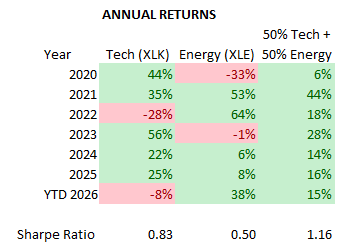

Under what conditions does equity market time series momentum (TSMOM) work and not work? In their June 2026 paper entitled “Boundaries of Time Series Momentum”, Matti Suominen and Erik Hjalmarsson examine performance of equity market TSMOM across ranges of three valuation metrics: cyclically adjusted price-to-earnings ratio (CAPE), dividend yield and term spread (difference between long-maturity and short-maturity Treasury instrument yields). They specify TSMOM as long (short) the market when past market return in excess of the risk-free rate over a specified lookback interval is positive (negative). They specify a Boundaries variable for predicting TSMOM performance as follows:

- Scale each of the CAPE, dividend yield and term spread to values between -1 and 1 as follows:

- Subtract from its 12-month average the past 10-year or 20-year minimum observation and divide the difference by the past 10-year or 20-year range (maximum minus minimum).

- Multiply results by two and subtract one.

- Compute a Boundaries variable as the square of the scaled term spread plus the square of scaled CAPE or scaled dividend yield.

For a given equity market, they construct a TSMOM index as an equal-weighted average of 25 time series momentum strategies, with lookback and investment intervals of 1, 3, 6, 9 or 12 months. They then explore how index returns interact with the Boundaries variable. Using the specified inputs and stock index returns during July 1927 through December 2024 for the U.S. and during January 1989 through December 2024 for a 20-country international sample, they find that: Keep Reading