Momentum Investing

Do financial market prices reliably exhibit momentum? If so, why, and how can traders best exploit it? These blog entries relate to momentum investing/trading.

March 10, 2020 - Momentum Investing, Sentiment Indicators, Strategic Allocation, Value Premium

“Verification Tests of the Smart Money Indicator” reports performance results for a specific version of the Smart Money Indicator (SMI) stocks-bonds timing strategy, which exploits differences in futures and options positions in the S&P 500 Index, U.S. Treasury bonds and 10-year U.S. Treasury notes between institutional investors (smart money) and retail investors (dumb money). Do these sentiment-based results diversify those for the Simple Asset Class ETF Momentum Strategy (SACEMS) and the Simple Asset Class ETF Value Strategy (SACEVS)? To investigate, we look at correlations of annual returns between variations of SMI (no lag between signal and execution, 1-week lag and 2-week lag) and each of SACEMS equal-weighted (EW) Top 3 and SACEVS Best Value. We then look at average gross annual returns, standard deviations of annual returns and gross annual Sharpe ratios for the individual strategies and for equal-weighted, monthly rebalanced portfolios of the three strategies. Using gross annual returns for the strategies during 2008 through 2019, we find that: Keep Reading

January 14, 2020 - Momentum Investing, Strategic Allocation, Technical Trading

How can investors suppress the downside of trend following strategies? In their July 2019 paper entitled “Protecting the Downside of Trend When It Is Not Your Friend”, flagged by a subscriber, Kun Yan, Edward Qian and Bryan Belton test ways to reduce downside risk of simple trend following strategies without upside sacrifice. To do so, they: (1) add an entry/exit breakout rule to a past return signal to filter out assets that are not clearly trending; and, (2) apply risk parity weights to assets, accounting for both their volatilities and correlations of their different trends. Specifically, they each month:

- Enter a long (short) position in an asset only if the sign of its past 12-month return is positive (negative), and the latest price is above (below) its recent n-day minimum (maximum). Baseline value for n is 200.

- Exit a long (short) position in an asset only if the latest price trades below (above) its recent n/2-day minimum (maximum), or the 12-month past return goes negative (positive).

- Assign weights to assets that equalize respective risk contributions to the portfolio based on both asset volatility and correlation structure, wherein covariances among assets adapt to whether an asset is trending up or down. They calculate covariances based on monthly returns from an expanding (inception-to-date) window with baseline 2-year half-life exponential decay.

- Impose a 10% annual portfolio volatility target.

Their benchmark is a simpler strategy that uses only past 12-month return for trend signals and inverse volatility weighting with annual volatility target 40% for each asset. Their asset universe consists of 66 futures/forwards. They roll futures to next nearest contracts on the first day of the expiration month. They calculate returns to currency forwards using spot exchange rates adjusted for carry. Using daily prices for 23 commodity futures, 13 equity index futures, 11 government bond futures and 19 developed and emerging markets currency forwards as available during August 1959 through December 2017, they find that: Keep Reading

December 26, 2019 - Momentum Investing

What is the best way to balance crash protection and false alarms for intrinsic, also called absolute or time series, momentum strategies that are long (short) an asset when its return over a specified past interval is positive (negative)? In their November 2019 paper entitled “Momentum Turning Points”, Ashish Garg, Christian Goulding, Campbell Harvey and Michele Mazzoleni investigate blending slow and fast intrinsic momentum signals with various weights on each (adding to one) to identify the best way to handle reversals in trend direction. They specify a slow (fast) signal as that derived from past 12-month (1-month) excess return. They define four market states: (1) Bull (slow and fast signals both non-negative); (2) Correction (slow signal non-negative and fast signal negative); (3) Bear (slow and fast signals both negative); and, (4) Rebound (slow signal negative and fast signal non-negative). They first consider static weights in increments of 25% for slow and fast signals. They then consider a dynamic strategy with slow and fast signal weights that differ for Correction and Rebound states as identified with monthly data. They test usefulness of the dynamic strategy by optimizing weights with historical returns and then evaluating performance of these weights out-of-sample. While focusing on the U.S. stock market, they test robustness of findings across other developed country equity markets. Using monthly excess returns for the U.S. value-weighted stock market since July 1926 and for 10 other developed stock markets since February 1980, all through December 2018, they find that:

Keep Reading

December 20, 2019 - Animal Spirits, Individual Investing, Momentum Investing

Is retail trading a reliable driver of U.S. stock momentum? In his November 2019 paper entitled “Retail Trading and Momentum Profitability”, Douglas Chung investigates interactions across stocks between current proportion of retail trading and future momentum returns. Specifically, for each month and for each of two recent stock samples, he:

- Sorts stocks into fifths (quintiles) by current proportion of retail trading.

- Within each proportion-of-retail-trading quintile:

- Sorts stocks into sub-quintiles by return from 12 months ago to one month ago.

- Calculates average next-month returns for an equal-weighted momentum portfolio that is long (short) the sub-quintile of stocks with the highest (lowest) past returns. He also considers other portfolio weighting schemes.

- Measures alphas of these returns based on various widely accepted single-factor and multi-factor models of stock returns.

He next tests whether proportion of retail trading relates to a gambling motive (lottery trading) by constructing a stock lottery index from inverse of stock price, idiosyncratic volatility, idiosyncratic skewness and recent maximum daily return. In other words, he examines whether the lottery index value for a stock is a proxy for its proportion of retail trading. Using daily data for all NYSE retail orders during March 2004 through December 2014, for small NYSE trades of U.S. common stocks (a proxy for retail trading) during January 1993 through July 2000 and for lottery index inputs during 1940 through 2016, he finds that: Keep Reading

December 17, 2019 - Equity Premium, Momentum Investing, Value Premium, Volatility Effects

Do both the long and short sides of portfolios used to quantify widely accepted equity factors benefit investors? In their November 2019 paper entitled “When Equity Factors Drop Their Shorts”, David Blitz, Guido Baltussen and Pim van Vliet decompose and analyze gross performances of long and short sides of U.S. value, momentum, profitability, investment and low-volatility equity factor portfolios. The employ 2×3 portfolios, segmenting first by market capitalization into halves and then by selected factor variables into thirds. The extreme third with the higher (lower) expected return constitutes the long (short) side of a factor portfolio. When looking at just the long (short) side of factor portfolios, they hedge market beta via a short (long) position in liquid derivatives on a broad market index. Using monthly returns for the specified 2×3 portfolios during July 1963 through December 2018, they find that:

Keep Reading

December 6, 2019 - Animal Spirits, Equity Premium, Fundamental Valuation, Momentum Investing

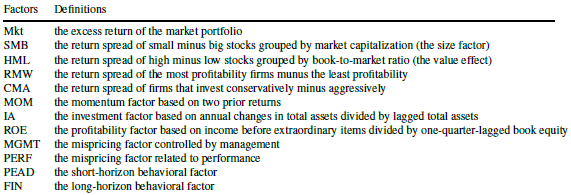

Which equity factors from among those included in the most widely accepted factor models are really important? In their October 2019 paper entitled “Winners from Winners: A Tale of Risk Factors”, Siddhartha Chib, Lingxiao Zhao, Dashan Huang and Guofu Zhou examine what set of equity factors from among the 12 used in four models with wide acceptance best explain behaviors of U.S. stocks. Their starting point is therefore the following market, fundamental and behavioral factors:

They compare 4,095 subsets (models) of these 12 factors models based on: Bayesian posterior probability; out-of-sample return forecasting performance; gross Sharpe ratios of the optimal mean variance factor portfolio; and, ability to explain various stock return anomalies. Using monthly data for the selected factors during January 1974 through December 2018, with the first 10 (last 12) months reserved for Bayesian prior training (out-of-sample testing), they find that: Keep Reading

November 18, 2019 - Momentum Investing

Do U.S. equity exchange-traded funds (ETF) exhibit long-term momentum? In their October 2019 paper entitled “ETF Momentum”, Frank Li, Melvyn Teo and Chloe Yang investigate future performance of U.S. equity ETFs sorted on multi-year past returns. Each month starting August 2004, they:

- Sort selected ETFs into tenths (deciles) based on returns over the past two, three or four years, with focus on three years.

- Reform an equal-weighted (EW) or value-weighted (VW) portfolio that is long (short) the decile with the highest (lowest) past returns, with focus on value-weighted.

They then evaluate performances of deciles and long-short portfolios based on raw return, 4-factor (adjusting for market, size, book-to-market and momentum) alpha and 5-factor (replacing momentum with profitability and investment) alpha. Using monthly returns, market capitalizations and net asset values for all U.S. equity ETFs with capitalizations greater than $20 million and share price greater than one dollar during August 2000 through June 2018, they find that: Keep Reading

November 15, 2019 - Fundamental Valuation, Momentum Investing

Does including a measure of asset valuation as a qualifier improve the performance of intrinsic (absolute or time series) momentum? In their October 2019 paper entitled “Carry and Time-Series Momentum: A Match Made in Heaven”, Marat Molyboga, Junkai Qian and Chaohua He investigate modification of an intrinsic momentum strategy as applied to futures using the sign of the basis (difference between nearest and next-nearest futures prices) for four asset classes: equity indexes (12 series), fixed income (18 series), currencies (7 series) and commodities (28 series). Their benchmark intrinsic momentum strategy is long (short) assets with positive (negative) returns over the last 12 months, with either: (1) equal allocations to assets, or (2) dynamic allocations that each month target 40% annualized volatility for each contract series. The modified strategy limits long (short) positions to assets with positive (negative) prior-month basis. They account for frictions due to portfolio rebalancing and rolling of contracts using cost estimates from a prior study. They focus on Sharpe ratio to assess strategy performance. Using monthly returns for 65 relatively liquid futures contract series during January 1975 through December 2016, they find that:

Keep Reading

November 5, 2019 - Momentum Investing, Strategic Allocation

The Simple Asset Class ETF Momentum Strategy (SACEMS) each month picks the one, two or three of nine asset class proxies with the highest cumulative total returns over a specified lookback interval. A subscriber proposed instead using the optimal intrinsic (time series or absolute) momentum lookback interval for each asset rather than a common lookback interval for all assets. SACEMS and the proposed approach represent different beliefs (which could both be somewhat true), as follows:

- Many investors adjust asset class allocations with some regularity, such that behaviors of classes are important and coordinated.

- Many investors switch between specific asset classes and cash with some regularity, such that each class may exhibit distinct times series behavior.

To investigate, we consider two ways to measure intrinsic momentum for each asset class proxy:

- Correlation between next-month return and average monthly return over the past one to 12 months. The lookback interval with the highest correlation has the strongest (linear) relationship between past and future returns and is optimal.

- Intrinsic momentum, measured as compound annual growth rate (CAGR) for a strategy that is in the asset (cash) when its total return over the past one to 12 months is positive (zero or negative). The lookback interval with the highest CAGR is optimal.

We use the two sets of optimal lookback intervals (optimization-in-depth) to calculate momentum for each asset class proxy as its average monthly return over its optimal lookback interval. We then compare performance statistics for these two alternatives to those for base SACEMS, focusing on: gross CAGR for several intervals; average gross annual return; standard deviation of annual returns; gross annual Sharpe ratio; and, gross maximum drawdown (MaxDD). Using monthly dividend-adjusted prices for SACEMS asset class proxies during February 2006 through September 2019, we find that:

Keep Reading

October 25, 2019 - Economic Indicators, Momentum Investing

A reader requested review of the Decision Moose asset allocation framework. Decision Moose is “an automated stock, bond, and gold momentum model developed in 1989. Index Moose uses technical analysis and exchange traded index funds (ETFs) to track global investment flows in the Americas, Europe and Asia, and to generate a market timing signal.” The trading system allocates 100% of funds to the index projected to perform best. The site includes a history of switch recommendations since the end of August 1996, with gross performance. To evaluate Decision Moose, we assume that switches and associated trading returns are as described (out of sample, not backtested) and compare the returns to those for dividend-adjusted SPDR S&P 500 (SPY) over the same intervals. Using Decision Moose signals/performance data and contemporaneous SPY prices during 8/30/96 through 9/30/19 (23+ years), we find that: Keep Reading